#CLARITY Act

New PAC Launches to Protect DeFi Developers

Crypto's political machine keeps getting bigger, and now it's getting more specialized. A brand-new political action committee called Defend Developers PAC launched Wednesday with a pretty specific mandate: back the lawmakers who are willing to fight for legal protections for the people actually writing blockchain code.

The group describes itself as the first hybrid PAC focused exclusively on American crypto developers, DeFi builders, and blockchain technologists. It was federally registered just last month, and its founders say they plan to put six figures or more into dozens of congressional races before November.

Who's Behind It

The PAC was founded by Gavin Zavatone, who also serves as policy lead at the DeFi Education Fund, a trade group that lobbies for DeFi-friendly regulation in Washington. The board pulls together names from across the industry: Uniswap Labs, the Solana Policy Institute, the American Innovation Project, and Orca Creative all have representation.

"We plan to raise and contribute more than six figures across dozens of key races in the midterms, because crypto technologists deserve champions in Congress who will go to bat for them," Zavatone said in a statement. No specific dollar amounts have been disclosed yet regarding the PAC's initial funding, but the stated plan is to draw contributions primarily from crypto founders, CEOs, and builders who have a direct stake in how DeFi regulation shakes out.

A Different Kind of Strategy

What sets Defend Developers apart is who it plans to back. Rather than looking for new candidates to anoint or taking shots at incumbents it dislikes, the group says it will focus its money on lawmakers who are already in Congress and already working on these issues. The theory is that incumbent support carries more weight in shaping actual legislation, especially when that legislation, namely the Clarity Act, is still actively being negotiated.

Developer protections have emerged as one of the trickier sticking points in the Clarity Act talks. The bill, which cleared the Senate Banking Committee earlier this year with bipartisan support, still needs to navigate several unresolved issues before it can reach a floor vote. Defend Developers PAC is betting that funneling money toward lawmakers who are already shaping those negotiations is smarter than trying to build from scratch.

A Crowded Field With One Clear Leader

Let's be clear about where Defend Developers sits in the broader crypto PAC landscape: it's not challenging Fairshake anytime soon. The industry's dominant super PAC, backed by Coinbase, Andreessen Horowitz, and Ripple, entered 2026 with north of $191 million in its war chest and has been racking up wins all cycle.

Just this week, Fairshake went 11-for-11 in Tuesday's primaries, backing nine Democratic House candidates in California, one in New Jersey, and Republican Senator Mike Rounds in South Dakota. All of them won. That follows a dominant performance in Texas last week, where crypto-aligned PACs spent more than $9 million across both parties and delivered a notable defeat to Rep. Al Green, a longtime critic of the industry, who lost his seat to Christian Menefee. Fairshake has spent $6.5 million on that race alone.

The new PAC also doesn't yet rival mid-tier players like the Fellowship PAC, which is tied to Tether, or the Digital Freedom Fund, connected to Tyler and Cameron Winklevoss at Gemini. But it's also not trying to. Defend Developers is playing a narrower game, and that might actually be the point.

What To Expect Heading Into November

The launch of another crypto PAC is one more sign of just how much the industry has matured as a political force. Lobbying groups have reportedly spent well over $271 million swaying electoral outcomes since the start of 2026 alone, largely through advertising. The latest addition to that landscape signals that crypto's political operation is growing more specialized, not just bigger.

The Blockchain Association also organized a Washington fly-in this week, bringing former national security and law enforcement officials to Capitol Hill for briefings with staff from roughly 18 Senate offices. A virtual town hall with lawmakers was also scheduled for Thursday. The coordination across lobbying groups, PACs, and trade organizations is about as sophisticated as it's ever been.

With prediction markets roughly split on which party controls Congress after November, the crypto industry's bipartisan strategy is starting to look less like a compromise and more like a deliberate hedge. The general election stakes are high, and groups like Defend Developers are clearly trying to make sure that regardless of who wins, there will be friendly faces in the room when the serious DeFi legislation gets written.

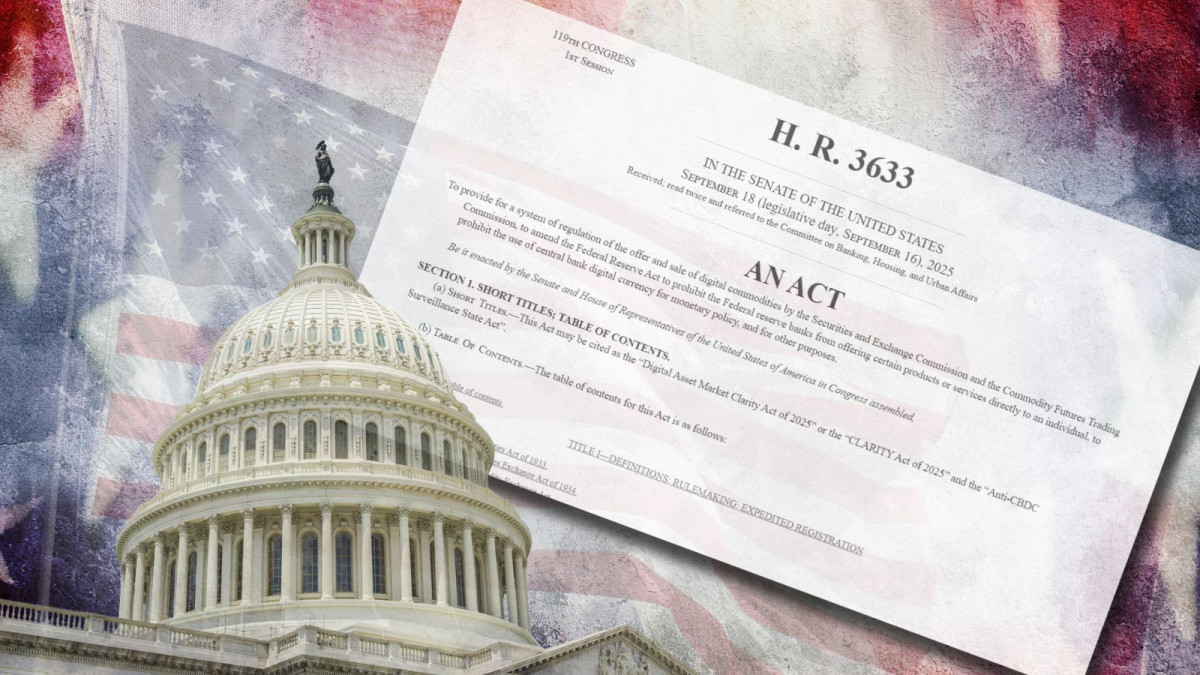

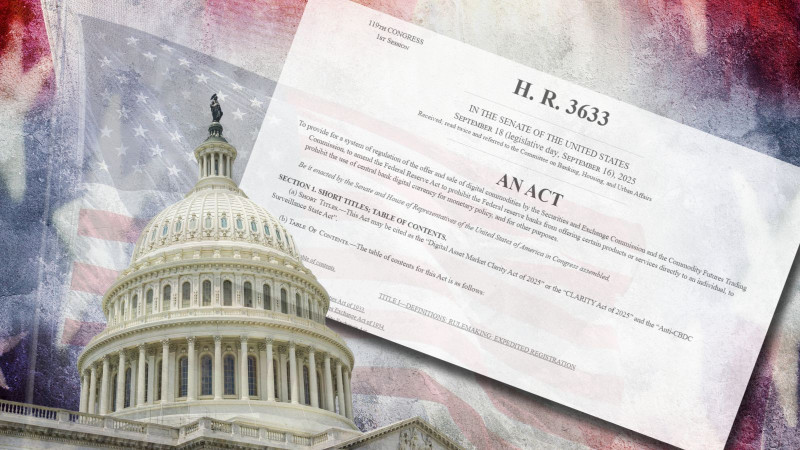

Clarity Act Advances, Massive Optimism for Digital Assets

After months of gridlock and four hours of pointed debate, the Senate Banking Committee voted 15-9 to advance the Clarity Act, sending one of the most consequential pieces of financial legislation in recent memory toward a full Senate floor vote. Two Democrats joined all Republicans on the panel in support, a small but symbolically meaningful show of bipartisan backing that industry advocates say could prove decisive when the bill eventually needs 60 votes to pass the full chamber.

For the digital asset industry, the vote felt like a long time coming. The bill, formally titled the Digital Asset Market Clarity Act of 2025, has been kicking around Capitol Hill for well over a year. The fact that it cleared committee at all, given the partisan atmosphere that dominated much of Thursday's hearing, was seen by many in the space as a genuine win.

Rules of the Road, Finally

At its core, the Clarity Act tries to solve a problem that has dogged the crypto industry since its earliest days: nobody could quite agree on who was in charge. The SEC and the CFTC have spent years in an uneasy standoff over which agency has jurisdiction over which digital assets, leaving companies in legal limbo and pushing some development offshore. The bill would draw a cleaner line, classifying digital assets as either securities or commodities and assigning oversight accordingly.

The market responded before the committee even finished voting. Coinbase surged more than 8% on the session, as investors bet that regulatory clarity could finally unlock the broader institutional participation that has been sitting on the sidelines. Galaxy Digital climbed over 6%. Strategy, the largest corporate bitcoin holder, was up 7%. Bitcoin itself ground higher, hitting session highs near $81,500.

"For too long, regulatory uncertainty has sent talent, investment, and innovation overseas, strengthening foreign competitors while leaving American builders without the certainty they need to compete," said Blockchain Association CEO Summer Mersinger, who called the committee vote a "defining moment." Ripple CEO Brad Garlinghouse was blunter: "If the largest economy in the world is going to lead on crypto, and it must, this is the moment."

Still Some Runway Ahead

Thursday's vote was a milestone, but it is not the finish line. The bill still needs to be reconciled with a separate version approved by the Senate Agriculture Committee, and the full Senate will require 60 votes to pass it, meaning a significant number of Democrats will have to come on board. The House passed its own version of the legislation last year, so the two chambers will also need to hammer out a unified text before anything heads to President Trump's desk.

The largest outstanding issue is an ethics provision intended to limit government officials, including the president, from profiting off crypto. Democrats have made clear they will not move forward without some version of it, while White House crypto adviser Patrick Witt has said the administration will not tolerate language targeting a specific officeholder. Both sides appeared at least open to finding common ground, with Cody Carbone of the Digital Chamber telling reporters that a deal on the ethics provision is likely a prerequisite for getting the bill to a floor vote at all. The window, several lawmakers noted, is probably August.

A Framework Built to Last

What makes the Clarity Act different from the patchwork of guidance and enforcement actions that have defined crypto policy for the past decade is its ambition. It does not try to pigeonhole digital assets into frameworks designed for equities or futures contracts decades ago. It builds something new, with defined registration pathways for digital commodity exchanges, brokers, and dealers, as well as clear definitions covering blockchain applications, protocols, and smart contracts.

Ji Hun Kim, CEO of the Crypto Council for Innovation, put it plainly after the vote: "Clear durable rules will help drive greater institutional and retail adoption, support innovation, create more high quality jobs in the U.S., protect Americans, and ensure that our country leads when it comes to digital assets policy and innovation."

The GENIUS Act, which passed the full Senate 68-30 last year, showed that comprehensive crypto legislation can attract broad support once the details are sorted. The Clarity Act is a harder lift, covering more ground and touching more competing interests. But Thursday's committee vote suggests the political will is there, and the industry is watching closely.

"Durable, lasting digital asset policy must be built on a bipartisan foundation," Mersinger added. By that measure, the Clarity Act is not finished yet. But for the first time in a long while, it looks like it might actually get there.

Why This Matters for the Future of Digital Assets

Let's be clear about all of this: Thursday was a great day for anyone who believes that digital assets have a meaningful role to play in the future of finance. I am certainly one of those. Not because the Clarity Act is perfect, and not because it's done, but because it signals something important that has been missing for years: the U.S. government is starting to treat this industry like it's here to stay.

The case for optimism goes beyond this single vote. The GENIUS Act passing 68-30 last year proved that stablecoin legislation could attract real bipartisan support. Institutional investment in Bitcoin ETFs has steadily matured. Major financial players who once dismissed crypto as a fringe asset are now building infrastructure around it. The underlying technology, particularly in DeFi and tokenization, keeps advancing regardless of what Washington does. What regulation does is create the conditions for all of that to compound. It clears the path for pension funds, endowments, and large asset managers who have been sitting on the sidelines waiting for legal certainty before committing serious capital.

That said, the Senate still has to close the deal, and that is not a given. The remaining sticking points on the ethics provision and law enforcement concerns are real, not just noise. Lawmakers like Senator Kirsten Gillibrand have been consistent that they will not deliver Democratic votes without meaningful conflict-of-interest guardrails, and that is a fair position. The 60-vote threshold means the bill needs to be genuinely bipartisan, not just technically so.

On timing, the realistic window is narrower than it might appear. Industry insiders, including Cody Carbone of the Digital Chamber, have pointed to August as a likely deadline if the bill is to move this year. Congress typically slows through the fall ahead of elections, and the legislative calendar fills up fast. That gives negotiators roughly ten to twelve weeks to reconcile the two committee versions, finalize the ethics language, and lock down the 60 votes needed for a floor vote. It is achievable, but it requires both parties to decide they want a deal more than they want a talking point.

If it does pass, the long-term impact will be substantial. Clear rules attract capital. Capital attracts builders. Builders create products that bring in users. That cycle, running inside a legitimate regulatory framework and anchored in the world's largest economy, is how digital assets stop being a niche and become infrastructure. You know...that "mass adoption" that people have been talking about for years? Well, this could be it. It might not look like how we all imagined, but what ever really does? Thursday was one huge step in that direction. The Senate now needs to finish what it started and we need to come together to make sure they all know that they need to do just that. Let's get it done.

Senate Strikes Stablecoin Yield Deal, Clearing Path for the CLARITY Act

Something shifted in Washington on Friday, and the people who have been watching the CLARITY Act back and forth for months could feel it. Two key lawmakers, Republican Thom Tillis of North Carolina and Democrat Angela Alsobrooks of Maryland, reached an agreement in principle on one of the most stubbornly contested provisions in the bill: stablecoin yield. It is the kind of deal that, when the details finally shake out, may well be remembered as the moment the United States stopped kicking the crypto regulatory can down the road.

The news broke late Friday and was first reported by Politico. Senator Alsobrooks confirmed it plainly. "Sen. Tillis and I do have an agreement in principle," she said. "We've come a long way. And I think what it will do is to allow us to protect innovation, but also gives us the opportunity to prevent widespread deposit flight." The White House's crypto executive director, Patrick Witt, called it a "major milestone" and added that more work remains, but that progress toward passing the CLARITY Act was now real and tangible.

Senator Cynthia Lummis, the Wyoming Republican who chairs the Senate Banking Committee's crypto subcommittee and has been one of the most tireless advocates for this legislation, marked the occasion in her own way. She posted a photo on X of a "yield" sign. No caption needed.

The Stablecoin Yield Standoff, Explained

For months, the stablecoin yield question was the immovable object blocking the CLARITY Act from getting its Senate Banking Committee hearing.

The GENIUS Act, signed into law by President Trump in July 2025, prohibits stablecoin issuers from paying interest directly to holders. The intent was to prevent stablecoins from functioning as de facto bank deposit accounts, which would put them in direct competition with traditional savings products and, as the American Bankers Association argued loudly, threaten deposit flows into community banks. The concern: if Coinbase or another platform could offer users 4% on their dollar-pegged tokens simply for holding them, why would anyone keep money in a checking account?

The problem is that the GENIUS Act only covered issuers. It left a gap for third-party platforms that might offer rewards to customers who hold stablecoins on their systems. The ABA saw this as a loophole and spent months in Washington lobbying to close it. Crypto companies, for their part, said those rewards programs were fundamentally different from deposit interest and should be allowed.

Section 404 of the Senate Banking Committee's draft tried to thread this needle. It prohibits digital asset service providers from paying interest or yield "solely in connection with the holding of a payment stablecoin," while explicitly allowing "activity-based" rewards tied to transactions, payments, platform use, loyalty programs, liquidity provision, and other behaviors. The distinction is real: a reward for moving money through a system is not the same thing as interest paid for parking money in one.

Senator Mike Rounds, a South Dakota Republican on the Banking Committee, captured the nuance at an ABA summit earlier this month: rewards cannot be simply about how much money sits in an account, but they might reasonably be tied to how active that account is. "We're trying to reflect that in the discussions," he said.

Lummis had suggested the final compromise would disallow anything that "sounds like banking product terminology" and bar rewards tied to the size of a user's balance. Coinbase CEO Brian Armstrong, whose withdrawal of support in January helped torpedo a scheduled markup hearing, has been described by Lummis as "really pretty good about being willing to give on this issue."

From 99% to Done

The past week has been a rapid acceleration. As recently as Thursday, sources familiar with the situation described the stablecoin yield issue as being on the verge of resolution. A closed Senate Republican meeting on Wednesday, attended by White House crypto council director Patrick Witt, produced what Lummis told reporters afterward were significant breakthroughs, with "major light bulbs" switched on among the participants.

FinTech Weekly, which has closely tracked the legislative calendar, reported that stablecoin yield negotiations were "99% of the way to resolution" coming out of that meeting. The digital asset provisions of the bill more broadly were described as being in a "good place." The remaining friction, sources said, was not technical but political, specifically around whether community bank deregulation provisions might be attached to the CLARITY Act as part of a broader legislative trade.

Then came Friday's agreement. "We've come a long way," Alsobrooks told Politico, with a formality that understated just how much ground has been covered since January, when the scheduled markup hearing collapsed under the weight of over 100 proposed amendments and an industry revolt over the yield language.

What Comes Next and Why the Timeline Matters

An agreement on yield does not mean the CLARITY Act is done. Several other issues need resolution, decentralized finance remains a live debate, and the bill still needs to clear the Senate Banking Committee before it can go to a full Senate vote. After that, it must be reconciled with the version that passed the Senate Agriculture Committee in January. And before the President can sign it, that combined Senate text has to be reconciled with the House-passed version from July 2025.

But the clock is ticking here. Senate Majority Leader John Thune controls the floor calendar, and it is crowded. Unrelated fights, including the Republican voter-ID bill and ongoing debate over the situation in Iran, are competing for limited floor time. Haun Ventures CEO Katie Haun, in a CNBC interview Friday, put it directly: "The big question on the Clarity Act is, is Congress going to get a bill to the floor on time to vote?"

Lummis has said she expects a Banking Committee hearing in the latter half of April, after the Easter recess. Advocates have been hoping for a May resolution. Prediction markets are currently pricing the odds of the CLARITY Act being signed in 2026 at around 72%, according to FinTech Weekly. Treasury Secretary Scott Bessent has described passage as a spring 2026 target. Ripple CEO Brad Garlinghouse has put the odds at 80 to 90%.

JPMorgan analysts have described CLARITY Act passage by midyear as a positive catalyst for digital assets, pointing to regulatory clarity, institutional scaling, and tokenization growth as the key drivers. The crypto industry committed nearly $150 million to the Fairshake political action committee in the current cycle and announced a $193 million war chest around the Agriculture Committee markup in January. The companies behind that spending are waiting.

What This All Means

The stakes of the CLARITY Act extend well beyond Senate procedure. Markets are waiting. Institutions that have been slowly building out crypto infrastructure, custody solutions, tokenized asset offerings, trading desks, need to know what the rules are before they can fully commit capital and resources. The SEC's interpretation helps, but as Atkins himself acknowledged, it is not a substitute for law.

The CLARITY Act, if signed, would give the CFTC clear jurisdiction over most digital asset spot markets, create a path to register exchanges and brokers, establish consumer protections with real enforcement teeth, and provide the kind of statutory framework that companies can build businesses around. It would, in the language of its Senate Banking Committee sponsors, establish the United States as the crypto capital of the world, not just by rhetoric but by law.

If the bill fails this year, the status quo continues. Crypto companies operate under regulatory uncertainty. The SEC retains broad discretion to treat digital assets as securities. Institutional adoption continues but without a clear statutory framework. And the crypto lobby, which has made clear it will treat failure as a political liability, turns its $193 million war chest into something that looks a lot more like electoral pressure.

Friday's agreement does not guarantee passage. It does something important though. It removes the single biggest substantive obstacle to moving forward. The stablecoin yield question, which derailed a January markup hearing and has consumed months of negotiations, now has a resolution in principle. The path ahead still has obstacles, but for the first time in a while, it looks like an actual path.

Senators Tillis and Alsobrooks just handed the crypto industry something it has been asking for since the last bull market: a credible signal that Washington is finally going to do its job. The deal is in principle, the details are not yet public, and there is still legislative work ahead. But after years of false starts, shelved bills, collapsed markup hearings, and agency standoffs, this is the moment the trajectory changed.

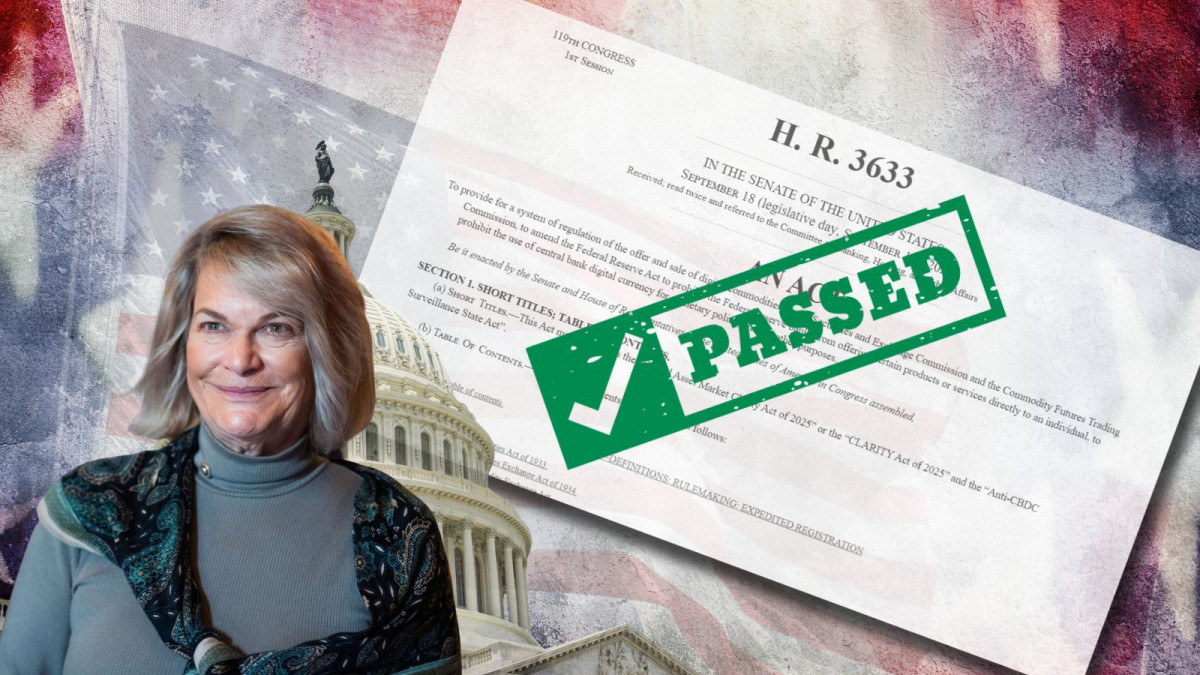

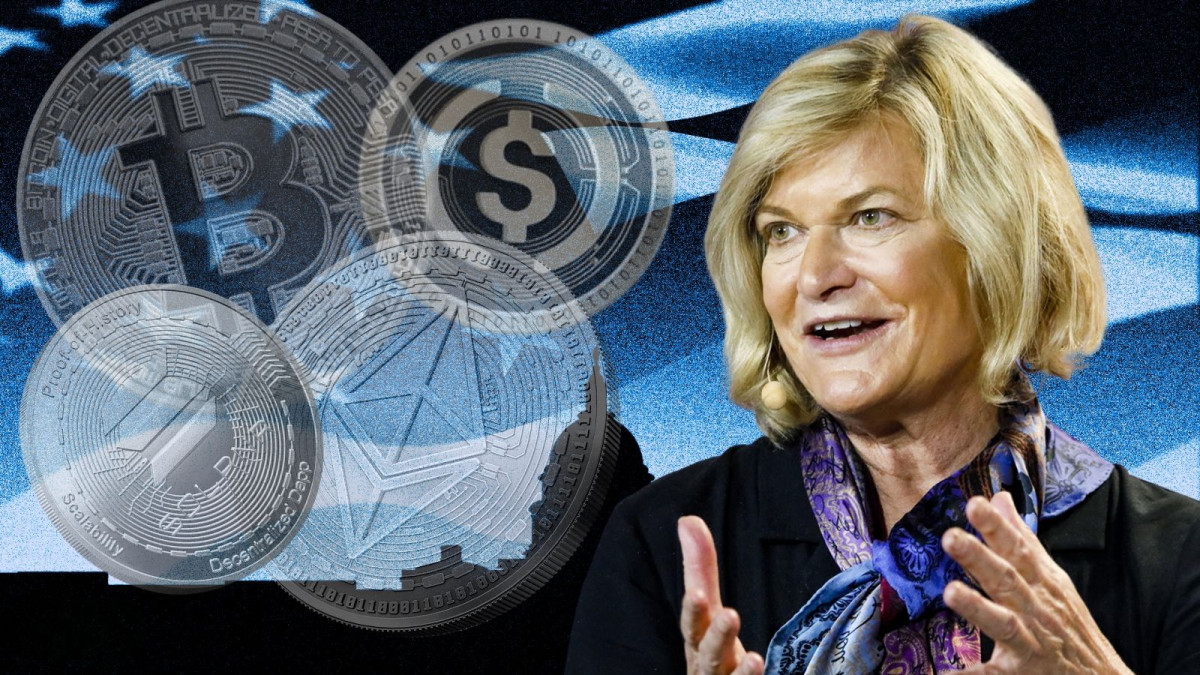

Lummis Says Crypto Market Structure Deal Is Near, Targets April Senate Committee Vote

Senator Cynthia Lummis, the Wyoming Republican who chairs the Senate Banking Committee's digital assets subcommittee and has spent the better part of two years shepherding the crypto industry's most ambitious legislative goal, walked into the Digital Chamber's DC Blockchain Summit and told a packed room what a lot of people in the industry had stopped expecting to hear.

"We think we've got it," she said. "We really are going to get it out of the banking committee in April."

That's a bigger deal than it might sound. The Digital Asset Market Clarity Act, the comprehensive crypto framework that cleared the House in a 294-134 bipartisan vote back in July 2025, has been grinding through Senate committees ever since, chewing through months of negotiations, a January markup that collapsed hours before it was scheduled to begin, and a dispute over stablecoin yield that managed to put banking lobbyists, crypto firms, and Democratic senators all at odds simultaneously. For a while, it looked like the whole thing might just quietly die before the 2026 midterms swallowed the calendar.

Apparently not, if Lummis is certain on the new deal being made.

The Stablecoin Yield Fight, Explained

To understand how we got here, it helps to understand the fight that almost killed this bill. After the House passed its version, the Senate Banking Committee got to work on its own draft. In January 2026, committee staff released a 278-page bill that took a firm stance: digital asset service providers could not offer interest or yield to users simply for holding stablecoin balances, though rewards or activity-linked incentives were still on the table.

Banking groups hated the carve-out. The American Bankers Association lobbied hard against any yield provision, arguing that if crypto platforms could pay customers to hold stablecoins, those customers might pull deposits from community banks. Coinbase, meanwhile, had built a profitable stablecoin rewards program and wasn't eager to see it legislated away. Coinbase CEO Brian Armstrong reportedly signaled opposition to an early compromise attempt, and within hours of the January 14 scheduled markup, committee leadership postponed it indefinitely.

That delay rattled markets, contributed to what analysts at CoinShares estimated as nearly $1 billion in crypto market outflows, and sent lobbyists back to their whiteboards.

The White House held at least three separate meetings over the following weeks to try to broker a deal. And now, Lummis says, a compromise has landed. Crypto platforms will not be able to offer rewards programs using language that sounds like banking products, whether that means using terms like "yield," "interest," or anything that ties payouts to how much a user holds rather than what they do.

"Anything that sounds like banking product terminology will not appear," Lummis said. She added that Armstrong had been "really pretty good about being willing to give on this issue," a notable shift from his earlier posture.

Senator Bernie Moreno, a Republican on the committee, confirmed the trajectory in a video statement at the same event, saying Senators Angela Alsobrooks, a Democrat, and Thom Tillis, a Republican, are in the final stages of the stablecoin talks alongside the White House. "Once they all sign off," Moreno said, it's "go time."

DeFi Disputes Quietly Shelved

DeFi was the other thing that kept lobbyists up at night. Decentralized finance protocols, which allow users to lend, borrow, and trade digital assets without going through a traditional intermediary, sit in a legal grey zone that both Democrats and Republicans approached with very different instincts.

Democrats wanted oversight that was on par with federally regulated financial firms. The crypto industry, somewhat predictably, wanted software developers and peer-to-peer activity protected from being treated as financial intermediaries. The House version of the bill had already tried to thread this needle by drawing a line between control and code: developers who publish or maintain software without directly handling customer funds would not be classified as financial intermediaries. Centralized entities that interact with DeFi protocols would face tailored requirements.

According to Lummis, those DeFi disagreements have been "put to bed." She didn't go into detail, but Senate Banking Committee materials describe the bill's approach as targeting control rather than code, and requiring risk management and cybersecurity standards for centralized intermediaries that touch DeFi, while leaving non-custodial software development out of scope.

The Ethics Problem Won't Go Away

Not everything is resolved. Senator Kirsten Gillibrand, a New York Democrat who has been one of Lummis's most consistent bipartisan partners on crypto legislation over the years, made clear at the same summit that there is still a major outstanding demand from her caucus.

Democrats want the bill to include an explicit ban on senior government officials personally profiting from the crypto industry. The reasoning for this is not very subtle, especially in heated partisanship of Washington these days: President Donald Trump and his family are tied to World Liberty Financial, a crypto platform that launched a stablecoin last year, and Trump's crypto-linked ventures have given Democrats a consistent line of attack.

"It's very important that we include this," Gillibrand said on Wednesday, adding that no government official in Congress or the White House should "get rich off their position and their knowledge base." Including such a restriction, she argued, would "unlock many more votes" from Democrats.

Lummis has previously said she took a compromise ethics provision to the White House and was rebuffed. Trump administration officials have repeatedly stated that the president's family's participation in digital asset businesses does not represent an inappropriate conflict of interests. The practical read from lobbyists: Republicans are unlikely to pass language that targets the leader of their own party.

The House bill, for its part, does include language specifying that existing ethics statutes already bar members of Congress and senior executive branch officials from issuing digital commodities during their time in public service. Whether that satisfies Democrats in the Senate is another matter.

Where the Bill Stands Procedurally

The legislative path from here still has a few moving parts. The Senate Agriculture Committee cleared its version of a crypto market structure bill, the Digital Commodity Intermediaries Act, in late January 2026. That bill covers the CFTC-related side of the regulatory picture, including commodity market oversight, exchange registration, and derivatives. It passed over the objections of Democratic members who tried and failed to push through a series of amendments.

The Senate Banking Committee bill, now expected to go through a markup in late April after the Easter recess, would handle the SEC-related provisions: investor protections, securities treatment of digital assets, and stablecoin regulation. Once it clears that committee, both Senate bills need to be reconciled and merged before heading to a full Senate floor vote. That combined version would then need to be aligned with the House-passed CLARITY Act before a single final bill could reach Trump's desk.

That's a lot of steps. Lummis, who announced in December that she will not seek re-election, seems acutely aware of the time pressure. "This may be our only chance to get market structure done," she posted on X on Wednesday. Moreno was even more pointed: "If we don't get the CLARITY Act passed by May, digital asset legislation will not pass for the foreseeable future."

The Senate's 2026 calendar is not working in the bill's favor. The midterm elections in November mean that floor time effectively closes for controversial legislation sometime around August, when lawmakers shift their attention to their races. A Senate majority that currently tilts Republican could flip to Democratic control after the vote, bringing new leadership to key committees and potentially shelving the bill for another cycle.

Making things more unpredictable, both parties are currently tangling over unrelated legislation and the U.S. involvement in the war in Iran, which threatens to consume floor time that crypto advocates would prefer to use for a market structure vote. Senate Majority Leader John Thune said as recently as last week that he did not expect the Banking Committee to pass the bill quickly. Whether that assessment holds is now up to the negotiators.

Prediction markets have priced the odds of the bill being signed into law in 2026 at around 72%, according to available data. JPMorgan analysts have described passage before midyear as a positive catalyst for digital assets, citing regulatory clarity, institutional scaling, and tokenization growth as key drivers. Ripple CEO Brad Garlinghouse has put his personal odds estimate even higher, at 80 to 90%.

Industry Money and Political Pressure

The stakes are reflected in the lobbying numbers. Total crypto industry lobbying expenditures topped $80 million in 2025. Fairshake, the industry's primary political action committee, had built a 2026 war chest of $193 million as of January, with Coinbase, Ripple, and Andreessen Horowitz each contributing $24 to $25 million in the second half of last year alone. The day before the Senate Agriculture Committee's January markup, Fairshake made that announcement public.

For all the money, the legislative process has been messier than the industry hoped. A bill that many expected to be done before year-end 2025 is now racing a midterm election clock, dependent on a handful of senators reaching agreement on provisions they've been arguing about for months, and navigating a Senate floor schedule that no one fully controls.

Lummis, for her part, sounded more confident than she has in months. "We're going to have this thing done, come hell or high water, before the end of the year," she told the crowd in Washington.

Whether the rest of the Senate, the White House, and the clock agree with her is the only question left.

Senators Race to Save the CLARITY Act With Stablecoin Yield Compromise

The room at the Marriott Marquis in Washington was full of community bankers on Tuesday, and Senator Angela Alsobrooks walked straight into the lion's den. Speaking at the American Bankers Association's annual Washington Summit, the Maryland Democrat delivered a message neither side particularly wanted to hear: everyone involved in the Digital Asset Market Clarity Act is going to have to walk away a little bit unhappy.

It was a remarkably candid thing to say in front of 1,400 people who have spent the better part of three months trying to kill the very provision that's been holding up the bill. But Alsobrooks, along with Republican Senator Thom Tillis of North Carolina, is now the central figure in a late-stage push to get the Clarity Act off the Senate Banking Committee floor and into an actual markup hearing before the legislative window closes for good.

The two senators confirmed Tuesday they're actively working on compromise language around stablecoin yield which keeps coming up as the main issue that has stalled what was supposed to be a landmark piece of crypto regulation.

A Bill In Limbo

The Digital Asset Market Clarity Act, or CLARITY Act, was supposed to have its Senate Banking Committee markup in January. That session got pulled at the last minute. The reason was stablecoin yield, specifically, amendments co-sponsored by Alsobrooks and Tillis that would restrict crypto firms from offering interest-like returns to customers who simply hold dollar-pegged digital tokens like USDC or USDT.

Banks had been lobbying hard against any provision that allowed that kind of reward. Their argument, which they've pushed loudly and repeatedly, is that stablecoins offering yield would function like bank accounts without the regulatory obligations of bank accounts. Executives at JPMorgan and Bank of America have cited Treasury Department modeling that suggested banks could lose up to $6.6 trillion in deposits if stablecoin yield programs went mainstream. Their argument is that it would starve the lending market and ultimately destabilize smaller regional banks that are particularly dependent on deposit funding.

The crypto industry dismisses most of that as fearmongering. Coinbase CEO Brian Armstrong called out the banking lobby publicly for what he characterized as anticompetitive blocking tactics and has pulled his support for the bill. In January at Davos, JPMorgan's Jamie Dimon reportedly told Armstrong he was, in quite colorful terms, wrong. The anecdote leaked out and became something of a symbol for just how personal this fight had gotten.

"We absolutely have to have these protections to prevent the deposit flight, but we're going to probably have to make some compromises." — Senator Angela Alsobrooks, D-Md.

The White House Steps In, Then Gets Rejected

By late February, the White House had grown impatient. Administration officials spent weeks brokering what they hoped would be an acceptable middle ground: allow stablecoin yield in limited contexts, particularly for activity tied to payments and transactions, while banning rewards on idle balances that look more like savings accounts. Crypto firms signed off on the framework. The banks did not.

On March 3rd, President Trump went public with his frustration. In a Truth Social post, he wrote that banks should not be trying to undercut the GENIUS Act or hold the CLARITY Act hostage, a shot across the bow that was notable both for its directness and for the fact that it did essentially nothing to move the American Bankers Association. Two days later, the ABA formally rejected the White House compromise anyway.

The March 1st deadline the White House had set for a resolution passed without published compromise text. Prediction markets, which had briefly priced Clarity Act passage at around 80% odds, fell back toward 55% as the stalemate hardened.

What the ABA rejection didn't do, however, is kill the legislation outright. Congress has passed bills over banking lobby opposition before. The question, as analysts and lobbyists have been pointing out all week, is whether there are enough Senate votes to do it again — and whether the calendar allows the time to find out.

Can We Get A Compromise?

The emerging deal that Alsobrooks and Tillis are proposing is a slimmed-down version of what the White House tried. Under the framework being discussed, yield on stablecoin holdings that closely resemble bank deposits would remain prohibited. But rewards tied to specific activities, like using stablecoins for payments or transactions on a given platform, could remain eligible for some form of customer incentive.

Both senators and many crypto advocates actually agree on the premise that pure holding rewards that look and function like savings account interest are a problem. The dispute is over where exactly to draw the line and how to define the categories well enough that neither side can game them after the fact.

Cody Carbone, the CEO of the Digital Chamber, said this week that Tillis has been very receptive to discussions about stablecoin yield and that he's optimistic the industry can get to yes on the bill. Summer Mersinger, the CEO of the Blockchain Association, noted that the White House weighing in on the negotiations and pushing banks to engage in good faith adds important momentum as talks continue.

The banks have maintained, publicly at least, that those assurances aren't enough. Their representatives at the ABA summit this week underlined again what they see as the risks of any yield loophole to their business model. The question of whether a markup hearing happens in late March or gets delayed again, depends entirely on whether Alsobrooks and Tillis can produce language the committee will actually vote on.

Timing Is An Issue

Behind every conversation about the Clarity Act this week is an unspoken anxiety about time. The Senate calendar is tight. Midterm elections are in November, and lawmakers will start dispersing from meaningful legislating sometime around May or June as campaign season accelerates. Unfortunately it seems, Congress prefers to stop working as they try to convince voters to keep them in their jobs. I know, makes perfect sense. If a markup isn't held and a floor vote isn't scheduled by sometime in April, realistically the bill is looking at the next Congress which could be a completely different party in power. And complicating things even more. Despite which party ends up winning the midterms, this could mean another 12 to 18 months of regulatory uncertainty for an industry that has been waiting years for a clear legal framework.

That timeline matters not just for the crypto industry's domestic ambitions, but for its competitive positioning globally. Under the European Union's MiCA framework, stablecoin yield products that are restricted or banned in the U.S. are already legal in European jurisdictions. Coinbase and others have been explicit about the risk that continued regulatory ambiguity in the U.S. will push capital, talent, and product development offshore. Trump made a version of the same argument in his Truth Social post last week, warning that failure would drive the industry to China.

There's also a strategic Bitcoin Reserve angle sitting quietly in the background. According to people familiar with the situation, the Trump administration has determined it needs congressional action to operationalize the planned Strategic Bitcoin Reserve that the president signed an executive order for over a year ago. That creates at least some White House motivation to see the broader Clarity Act process succeed.

What Happens Next

The Senate Banking Committee is targeting a late-March markup. Whether that happens depends on whether the Alsobrooks-Tillis compromise language satisfies enough members to call the vote. If it does, the bill would then need to be merged with a version that already passed the Senate Agriculture Committee on a party-line vote in late 2025. The combined text would require significant Democratic support to clear a full Senate vote, always a tall ask in the current politcal environment and the fact that seven Democratic senators have separately raised concerns about potential conflicts of interest involving senior government officials, including the president himself, who have financial ties to the crypto industry.

Even if the Senate acts, the bill still needs the House, where an earlier version of the CLARITY Act passed committee last year but has yet to reach the floor. The path to a signed law before November is narrow but not impossible. It requires the Senate Banking Committee to move in the next few weeks, the combined bill to hold together politically, and a Senate floor schedule that is packed with little wiggle room.

For the moment, all of it hinges on two senators and a room full of bankers in Washington D.C., trying to decide how much compromise is actually compromise and if they can all agree to leave a bit unhappy about the results for the greater good. Typically the best compromises do make both sides a bit unhappy. In Washington, that usually means the deal is closer than it looks. It also usually means it's harder than it sounds.

White House Calls Out Dimon on Stablecoin Yields

Washington's stablecoin standoff just got a whole lot more personal.

Patrick Witt, the executive director of the President's Council of Advisors for Digital Assets, publicly fired back at JPMorgan Chase CEO Jamie Dimon on Tuesday, calling his arguments about stablecoin yields misleading and, in Witt's own word, a "deceit."

The exchange marks one of the sharpest moments yet in a months-long tug-of-war between Wall Street and the White House over the future of digital asset regulation in America.

Dimon Draws a Line in the Sand

It started Monday, when Dimon went on CNBC and didn't mince words. His position was simple, if uncompromising: any platform holding customer balances and paying interest on them is functionally a bank, and should be regulated like one.

"If you do that, the public will pay. It will get bad," Dimon warned, arguing that a two-tiered system where crypto firms operate with fewer restrictions than banks is unsustainable.

Dimon suggested a narrow compromise: platforms could offer rewards tied to transactions. But he drew a clear line at interest-like payments on idle balances, saying, "If you're going to be holding balances and paying interest, that's a bank."

The list of obligations Dimon believes should apply is long, FDIC insurance, capital and liquidity requirements, anti-money laundering controls, transparency standards, community lending mandates, and board governance requirements. "If they want to be a bank, so be it," he said.

For Dimon, it's fundamentally about fairness. JPMorgan uses blockchain in its own operations, and the CEO was careful to frame his argument not as anti-crypto but as pro-competition on equal terms. "We're in favor of competition. But it's got to be fair and balanced," he said.

The White House Fires Back

Witt wasn't going to let that stand. In a post on X late Tuesday, he went directly at Dimon's framing, calling it deliberately misleading.

"The deceit here is that it is not the paying of yield on a balance per se that necessitates bank-like regulations, but rather the lending out or rehypothecation of the dollars that make up the underlying balance," Witt wrote. "The GENIUS Act explicitly forbids stablecoin issuers from doing the latter."

The argument gets at something technically important. What makes a bank risky, and therefore subject to heavy regulation, isn't that it pays interest. It's that banks take deposits and lend them back out, creating credit and the systemic risk that comes with it. If too many people want their money back at once, that's a bank run. Stablecoin issuers operating under the GENIUS Act must maintain reserves at a 1:1 ratio. There is no fractional reserve lending, no rehypothecation, no credit creation.

In Witt's view, stablecoin balances aren't deposits, and treating them as such misrepresents what's actually happening. He closed with a pointed equation: "Stablecoins ≠ Deposits."

President Donald Trump didn't stay quiet either. On Tuesday, he took to Truth Social with a message that made his position unmistakably clear.

"The U.S. needs to get Market Structure done, ASAP. Americans should earn more money on their money. The Banks are hitting record profits, and we are not going to allow them to undermine our powerful Crypto Agenda that will end up going to China, and other Countries if we don't get the Clarity Act taken care of," Trump wrote.

Senator Cynthia Lummis quickly reposted Trump's message, adding her own call to action: "America can't afford to wait. Congress must move quickly to pass the Clarity Act."

The same day Trump posted, a Coinbase delegation led by CEO Brian Armstrong visited the White House for talks. The timing was not subtle.

The Real Stakes: The CLARITY Act

To understand why this debate matters so much right now, you need to understand the legislation being held hostage by it.

The GENIUS Act, signed into law in July 2025, established the first federal framework for payment stablecoins. The CLARITY Act is its sequel: a broader market structure bill that would assign clear regulatory jurisdiction to the SEC and CFTC over the crypto industry, and is widely seen as the piece of legislation needed to unlock large-scale institutional participation in digital assets.

The bill cleared the House comfortably but has been mired in Senate gridlock since January, when the Senate Banking Committee indefinitely postponed a planned markup vote. The trigger was Coinbase withdrawing support over a proposed amendment that would have restricted stablecoin rewards for users.

That withdrawal, announced by CEO Brian Armstrong in a post on X the night before the scheduled committee vote, split the crypto industry. a16z crypto's Chris Dixon publicly disagreed, posting "Now is the time to move the Clarity Act forward." Kraken's co-CEO Arjun Sethi also pushed back, writing that "walking away now would not preserve the status quo in practice" and warning it "would lock in uncertainty and leave American companies operating under ambiguity while the rest of the world moves forward."

The stakes for Coinbase are concrete. Stablecoins contribute nearly 20% of Coinbase's revenue, roughly $355 million in the third quarter of 2025 alone, and most of USDC's growth is occurring on Coinbase's platform. Coinbase currently offers 3.5% yield on USDC, a figure most traditional bank accounts can't come close to matching.

Banks Are Scared, and They Have the Numbers to Show It

The banking lobby's concern isn't hypothetical. Banking trade groups, led by the Bank Policy Institute, have warned that unrestricted stablecoin yield could trigger deposit outflows of up to $6.6 trillion, citing U.S. Treasury Department analysis. Bank of America CEO Brian Moynihan put a similar figure forward, reportedly suggesting as much as $6 trillion in deposits, representing roughly 30-35% of all U.S. commercial bank deposits, could be at risk.

Stablecoins registered $33 trillion in transaction volume in 2025, up 72% year-over-year. Bernstein projects total stablecoin supply will reach approximately $420 billion by the end of 2026, with longer-run forecasts from Citi putting the market at up to $4 trillion by 2030. Those aren't niche numbers anymore. At that scale, deposit competition becomes a serious macroeconomic question.

The American Bankers Association and 52 state bankers' associations explicitly urged Congress to extend the GENIUS Act's yield prohibitions to partners and affiliates of stablecoin issuers, warning of deposit disintermediation.

The Bottom Line

What's playing out right now is a genuine philosophical disagreement about what money is and how it should be regulated, wrapped inside a very consequential legislative fight, a prize fight with Banks in one corner and Crypto in the other.

Dimon's argument is not frivolous. Banks are regulated as heavily as they are because of what they do with deposited money, and a world where consumers move trillions into yield-bearing crypto instruments held at lightly regulated platforms carries real risks. The history of financial crises is largely a history of regulatory arbitrage gone wrong.

But Witt's counter is also not frivolous. The GENIUS Act was designed specifically to prevent stablecoin issuers from doing the things that make banks dangerous. A fully reserved, non-lending stablecoin issuer is structurally different from a fractional reserve bank, and applying the same regulatory framework to both risks conflating two fundamentally different business models.

What's harder to square is that the banking lobby's intervention in the CLARITY Act seems, to many in the crypto world, less about prudential regulation and more about protecting market share. President Trump has not been subtle about that read, accusing banks of holding the CLARITY Act hostage to protect incumbent interests against crypto competition.

With the legislative window narrowing, Armstrong back at the White House, and Trump openly calling out the banking lobby by name, this standoff has reached the kind of inflection point where someone is going to have to blink. The question is whether either side is willing to do it before time runs out entirely.

Banks Are Drawing a Hard Line on Stablecoin Yield

Washington has spent the past several months talking about crypto clarity. What it got this week was something closer to a standoff.

At the center of the latest White House meeting between crypto executives and banking lobbyists was a surprisingly narrow issue that has turned into a major fault line: stablecoin yield.

On paper, the CLARITY Act is supposed to settle jurisdictional turf wars between regulators and create a workable framework for digital assets in the United States. In practice, negotiations have slowed to a crawl over whether stablecoin holders should be allowed to earn rewards.

Crypto companies came to the table expecting to negotiate. Bank representatives arrived with something closer to a red line.

The Yield Problem

Stablecoin yield sounds simple. Platforms offer incentives, rewards, or returns to users who hold dollar-backed tokens. Sometimes that comes from lending activity. Sometimes it comes from promotional programs. Structurally, it does not always look like a bank deposit.

Banks are not buying that distinction.

From their perspective, if consumers can hold tokenized dollars and earn a return without stepping inside the banking system, that looks a lot like deposit competition. And not just competition, but competition without the same regulatory burden.

Banks operate under capital requirements, liquidity ratios, deposit insurance rules, stress testing frameworks, and layers of federal oversight. Stablecoin issuers, even under proposed legislation, would not be subject to the same regime.

So the banking lobby’s position has been blunt. No yield. Not from issuers, not indirectly through affiliated programs, not in ways that replicate interest-bearing accounts.

The crypto side sees that as overreach.

Is This About Risk or About Control?

Publicly, banks frame their opposition as a financial stability issue. If large amounts of capital flow out of insured deposits and into stablecoins offering yield, that could shrink the deposit base that supports lending. In a stress scenario, they argue, the dynamic could amplify volatility.

There is logic there. Deposits are the backbone of bank balance sheets. Disintermediation is not a trivial concern.

But crypto executives are asking a quieter question. If the issue is really about safety, why push for a blanket prohibition rather than tighter guardrails? Why not cap yield structures, restrict how they are funded, or impose disclosure standards?

Why eliminate them entirely?

Some in the industry suspect the answer is competitive pressure. Stablecoins have already become critical plumbing for crypto markets, facilitating trading, settlement, and cross-border transfers. Add yield into the equation and they start to look even more like digital savings instruments.

That begins to encroach on traditional banking territory.

The Competitive Threat

Banks have historically tolerated crypto in its speculative corners. Trading tokens is volatile, niche, and largely outside the core consumer banking relationship.

Stablecoins are different. They are dollar-denominated. They are increasingly integrated into payment systems. They can move across borders faster than traditional rails. And they are programmable.

Now imagine those same tokens offering yield, even modest incentives. The psychological shift for consumers could be meaningful. Why leave idle cash in a checking account earning almost nothing if a tokenized version offers some return and similar liquidity?

To bankers, that is not innovation. That is deposit leakage.

And in a higher rate environment, where funding costs matter, deposit competition becomes more acute.

The Legislative Bottleneck

The CLARITY Act was supposed to resolve long-running disputes between regulators and provide certainty for digital asset firms operating in the United States. Instead, stablecoin yield has turned into the sticking point holding up broader progress.

White House officials have reportedly pressed both sides to find compromise language. So far, that compromise remains elusive.

Crypto firms argue that banning yield outright could push innovation offshore. Jurisdictions in Asia and parts of Europe are moving ahead with stablecoin frameworks that do not automatically prohibit reward structures. The fear in Washington’s crypto circles is that overcorrection could hollow out domestic competitiveness.

Banking groups counter that allowing yield would create a parallel banking system without equivalent safeguards.

The tension is not just technical. It is philosophical.

A Larger Question About Money

At its core, this debate is about who gets to intermediate digital dollars.

If stablecoins become widely used and allowed to offer returns, they could evolve beyond trading tools into mainstream financial instruments. That challenges the traditional hierarchy where banks sit at the center of deposit-taking and credit creation.

Banks are not opposed to digital dollars in theory. Many are experimenting with tokenization and blockchain infrastructure themselves. But they want those innovations inside the regulated banking perimeter, not outside of it.

Crypto companies, on the other hand, see decentralization and alternative rails as the point.

So when banks push to ban stablecoin yield entirely, the crypto industry reads it as more than prudence. It looks like an attempt to protect market share.

The Bottom Line

For now, negotiations continue. There is still political appetite in Washington to pass comprehensive crypto legislation, especially as digital asset markets remain a significant part of the financial system.

But unless lawmakers can thread the needle between stability concerns and competitive fairness, stablecoin yield could remain the issue that stalls everything else.

And that leaves an uncomfortable reality.

If the United States cannot decide whether digital dollars are allowed to earn a return, the market may decide elsewhere.

Why Banks Are Fighting So Hard Against Stablecoin Yield

There’s been a lot of language coming out of Washington lately about stablecoins.

Words like "prudence", "guardrails", and "financial stability" get thrown around whenever the CLARITY Act comes up. Coinbase recently pulled their support amid stablecoin issues in the same bill. But if you take a step back, it’s hard not to feel like something else is driving the intensity of the debate. Big banks don’t usually fight this hard over niche policy details unless there’s something material at stake.

Browsing the web, trying to find my next article for all of you, I came across a recent report from Standard Chartered’s digital assets research team, led by Geoff Kendrick, and it may just help to explain the fight a bit better.

A Forecast Banks Can’t Ignore

Kendrick’s research doesn’t treat stablecoins as a crypto sideshow. It treats them as a potential alternative home for real money, the kind of money that currently sits in checking and savings accounts. He actually estimated that $500 billion will move from bank deposits to stablecoins by 2028. The idea isn’t that everyone suddenly abandons banks. It’s subtler than that. Even a gradual shift of deposits into stablecoins changes the math for banks in ways they really don’t like. Funding becomes more expensive, liquidity assumptions get weaker, margins get squeezed. Those aren’t ideological concerns. Those are spreadsheet concerns. And spreadsheet concerns really make banks want to fight the issue.

But to understand the real threat to banks, you first have to better understand the business itself. Banks don’t just hold your money. They use it. Under fractional reserve banking, they keep only a slice and lend the rest out to earn interest for themselves. Sure, they'll keep that small portion of your deposit, but the majority gets reinvested through loans and other activities. That’s how they earn money and why they can afford to even pay any interest to you at all, even if it’s usually minimal.

This system works because deposits are assumed to be sticky. People don’t move their money often, and when they do, it usually stays within the banking system. Moving from one bank to another.

Stablecoins challenge that assumption. They make dollars mobile in a way they haven’t been before.

The Shift Is Coming

Right now, most stablecoins feel like tools, not destinations. They’re useful for transfers, trading, and crypto-native activity, but they’re not where most people park idle cash. Yield changes that. The moment a stablecoin starts paying something meaningfully better than a traditional savings account, the comparison becomes unavoidable. A digital dollar that moves instantly, works around the clock, and earns yield starts to look less like a crypto product and more like a better bank balance. That’s when stablecoins stop being adjacent to banking and start competing with it.

But, we're still talking mostly about crypto-native people. The real shift happens when stablecoins stop feeling like crypto at all, when they live inside apps people already trust and use every day. When you easily pay for your groceries on your phone without writing down that seed phrase for crypto that sits on a separate wallet that may or may not be linked to payments.

PayPal is already experimenting here. Their Paypal USD (PYUSD) exists inside a platform with hundreds of millions of users, and it already lets people move dollars instantly between PayPal and Venmo for free. That’s everyday payment stuff. It’s not a niche oracles or decentralized exchange use case. It’s peer to peer transfers in apps people use for rent, splitting bills, or sending money to family.

Cash App has also signaled support for stablecoin payments and more flexible money movement options, even if Bitcoin hasn’t become everyday cash yet. The point is simple: If stablecoins actually become integrated into the way regular people pay for things, save for short-term goals, and move money around, they stop being a "crypto thing” and become an alternative store of value and payment rail to banks.

That’s exactly the scenario a bank CFO would find unsettling.

Why the CLARITY Act Matters So Much

This is why the fight over stablecoin yield inside the CLARITY Act feels so charged. It’s not really about whether stablecoins should exist. That battle is already over. It’s about whether they’re allowed to become a true alternative to bank deposits. If yield stays restricted, stablecoins grow slowly and remain mostly transactional. If yield is allowed under a clear regulatory framework, they start to compete directly with how banks fund themselves. That’s a much bigger shift.

The Bottom Line

If you take Kendrick’s projections seriously, and I know that I do. I have been in this blockchain industry for a decade now. I have seen the shift from Silk Road and from not even being a second thought in Washington to being a presidential election policy issue and talked about at the highest levels of government, from sea to shining sea.

But pushback from banks does make sense. It’s not panic. It’s defense. Stablecoins that are easy to use, deeply integrated into everyday payment apps, how people spend their money, and capable of earning yield... threaten something fundamental. They threaten the quiet bargain where banks get cheap access to capital and customers accept low returns in exchange for convenience. Seen through that lens, the resistance to stablecoin yield isn’t surprising at all. It’s exactly what you’d expect when a new form of money starts to look a little too good at doing the job banks have always relied on to make money.

I know where I stand on the issue and I'm interested to know what you think. Do banks evolve, embrace stablecoins as inevitability or do they hold on to the old ways for dear life?

What the CLARITY Act Means for Crypto and Why It Matters So Much

If you have spent any real time building, trading, or working in crypto in the U.S., you already know the pattern. The rules are never fully clear. Guidance usually comes after the fact. And “compliance” often feels less like a checklist and more like a guessing game.

That is the environment the Digital Asset Market Clarity Act, better known as the CLARITY Act, is trying to change.

On January 15, 2026, the Senate Banking Committee is scheduled to hold a critical markup session on the bill. That might sound like inside-baseball legislative procedure, but it is not. A markup is where lawmakers decide what a bill really is. Language gets tightened. Loopholes get closed or widened. Entire sections can disappear.

For crypto, this is one of those moments where the future shape of U.S. regulation is actually being decided.

The problem CLARITY is trying to solve

Right now, crypto regulation in the U.S. is reactive.

The laws that exist were written long before blockchains, tokens, or decentralized networks. Regulators have mostly tried to force crypto into frameworks that were never designed for it, often relying on enforcement actions to define the rules retroactively.

CLARITY is an attempt to stop doing that.

The bill starts from a simple premise: not everything in crypto is the same, so it should not all be regulated the same way.

Launching a token to fund a network is not the same as trading that token years later. Writing open-source code is not the same as holding customer funds. Running a wallet is not the same as running an exchange.

Those distinctions sound obvious inside the industry. CLARITY tries to make them explicit in law.

Tokens are not frozen in time

One of the most important ideas in the bill is that a token’s legal treatment should not be locked forever to how it was first sold.

Under the current system, if a token was ever distributed in a way that looks like fundraising, it can carry securities risk indefinitely. Even if the network decentralizes. Even if the original team steps away. Even if the token functions more like a commodity than an investment.

CLARITY tries to separate:

-

The initial transaction, which may look like an investment contract

-

The token itself, once it is broadly distributed and actively used

That distinction matters because it opens the door to secondary markets operating without constant legal uncertainty, while still keeping guardrails around early fundraising.

What “mature blockchain” actually means

To make that transition possible, CLARITY introduces the concept of a mature blockchain system.

Stripped of legal language, the question is pretty straightforward: does anyone actually control this thing?

If a small group can still unilaterally change the rules, supply, or governance, regulators get more leverage. If control is meaningfully distributed and no one actor is calling the shots, the regulatory burden can ease.

The bill creates a certification process around this idea, with a defined window for regulators to challenge a claim of maturity.

This is one of the most debated sections of the bill. It is also one of the most important. The standard has to be real, but it also has to be achievable. Senate changes here could dramatically affect how useful the bill ends up being.

How token launches could work going forward

CLARITY does not remove oversight from token launches. Instead, it tries to make that oversight fit reality.

The bill allows certain token offerings to proceed under an exemption, but only with meaningful disclosures. Projects would need to explain things like:

-

How token supply and issuance work

-

What rights, if any, token holders have

-

How governance actually functions in practice

-

What the project plans to build and what risks exist

The shift here is away from clever legal gymnastics and toward plain-English transparency. For founders, that could mean fewer surprises and a clearer sense of what is expected.

Why exchanges are watching this so closely

For U.S. crypto exchanges, CLARITY is largely about secondary markets.

Today, listing a token can feel risky even if that same asset trades freely outside the U.S. The legal line between primary fundraising and secondary trading has never been cleanly drawn.

CLARITY tries to draw that line. If it holds, exchanges would finally have a framework designed specifically for spot crypto markets, instead of trying to fit into rules written for something else.

A bigger role for the CFTC

Another major shift is regulatory jurisdiction.

CLARITY gives the CFTC clear authority over spot markets for digital commodities, not just derivatives. It also creates new registration paths for exchanges, brokers, and dealers that are tailored to how crypto markets actually function.

Importantly, the bill pushes for speed. It directs the CFTC to create an expedited registration process, acknowledging that waiting years for clarity is not realistic in fast-moving markets.

DeFi, software, and where things get tricky

DeFi is where the bill walks a tightrope.

CLARITY says that people should not be treated as regulated intermediaries just for building or maintaining software, running nodes, providing wallets, or supporting non custodial infrastructure. It also makes clear that participating in certain liquidity pools, by itself, should not automatically trigger exchange-level regulation.

At the same time, fraud and manipulation laws still apply.

Supporters see this as long overdue recognition that infrastructure is not the same as custody or brokerage. Critics worry about edge cases, especially where front ends, admin controls, or governance tokens blur the lines.

This is an area where Senate edits could have outsized impact.

Federal rules versus state rules

The bill also leans toward stronger federal oversight and narrower state-by-state requirements in certain areas.

For companies, that means fewer conflicting regimes and lower compliance friction. For critics, it raises concerns about losing fast-moving state enforcement in an industry that still sees its share of bad actors.

That tension is not going away, and it will likely surface again during markup.

Self custody, explicitly protected

One of the clearest statements in CLARITY is its protection of self custody.

The bill explicitly affirms the right to hold your own crypto and transact peer to peer for lawful purposes. In an environment where indirect restrictions have been a constant fear, putting this into statute is not symbolic. It is structural.

Developers get some breathing room

CLARITY also addresses a long-running concern among builders.

The bill says that non-controlling developers and infrastructure providers should not be treated as money transmitters simply for writing code or publishing software, as long as they do not control user funds or transactions.

For many developers, this removes a quiet but persistent legal cloud that has hung over the industry.

Why January 15 is such a big deal

The January 15 markup is where all of this either becomes real or starts to unravel.

This is where lawmakers decide how strict the maturity standards are, how wide the DeFi exclusions go, how much authority regulators actually get, and whether the bill delivers usable clarity or just new gray areas.

If CLARITY moves forward in a recognizable form, it becomes the most serious attempt yet to give crypto a durable U.S. market structure. If it does not, the industry likely stays where it is now, building first and hoping the rules catch up later.

How you can get involved?

This is also the moment where voices outside Washington still matter.

Lawmakers are actively weighing feedback. Staffers are reading messages. Offices are tracking where their constituents stand. Silence gets interpreted as indifference, and indifference makes it easier for complex bills to stall or be watered down.

If you believe crypto should have clear rules instead of enforcement-by-surprise, this is the time to say so.

That means contacting your representatives. Find out who your representative is and where they stand on crypto policy. Tell them that market structure clarity matters. Explain why builders, users, and businesses need predictable rules to stay in the U.S. Explain why self custody, open infrastructure, and lawful innovation should be protected, not pushed offshore.

It also means supporting organizations that are trying to organize that voice.

One such organization is Rare PAC, a political action committee advocating for regulatory clarity, innovation, and economic opportunity powered by decentralized technologies. Rare PAC works to ensure that the United States remains a global leader in those decentralized technologies and supports candidates who are committed to building A Crypto Forward America.

Bills like CLARITY do not pass or fail in a vacuum. They pass because people show up, speak up, and make it clear that getting this right matters.

January 15 is not the end of the process, but it is one of the moments that will shape everything that comes after.