#crypto legislation

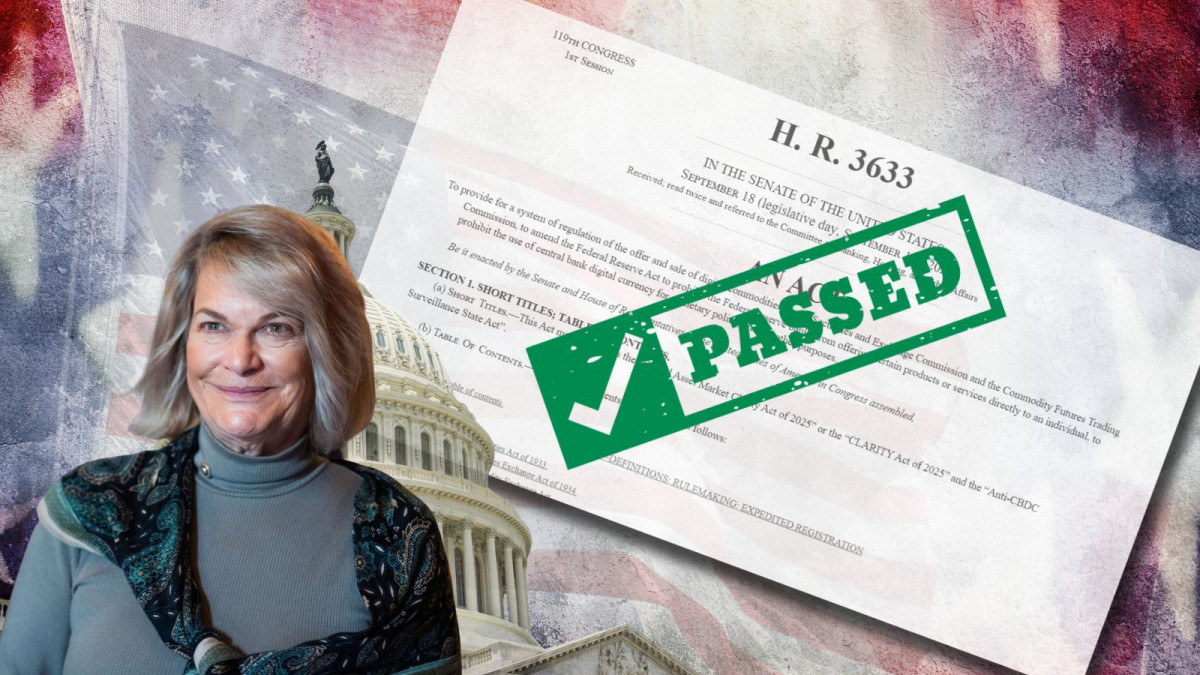

Clarity Act Advances, Massive Optimism for Digital Assets

After months of gridlock and four hours of pointed debate, the Senate Banking Committee voted 15-9 to advance the Clarity Act, sending one of the most consequential pieces of financial legislation in recent memory toward a full Senate floor vote. Two Democrats joined all Republicans on the panel in support, a small but symbolically meaningful show of bipartisan backing that industry advocates say could prove decisive when the bill eventually needs 60 votes to pass the full chamber.

For the digital asset industry, the vote felt like a long time coming. The bill, formally titled the Digital Asset Market Clarity Act of 2025, has been kicking around Capitol Hill for well over a year. The fact that it cleared committee at all, given the partisan atmosphere that dominated much of Thursday's hearing, was seen by many in the space as a genuine win.

Rules of the Road, Finally

At its core, the Clarity Act tries to solve a problem that has dogged the crypto industry since its earliest days: nobody could quite agree on who was in charge. The SEC and the CFTC have spent years in an uneasy standoff over which agency has jurisdiction over which digital assets, leaving companies in legal limbo and pushing some development offshore. The bill would draw a cleaner line, classifying digital assets as either securities or commodities and assigning oversight accordingly.

The market responded before the committee even finished voting. Coinbase surged more than 8% on the session, as investors bet that regulatory clarity could finally unlock the broader institutional participation that has been sitting on the sidelines. Galaxy Digital climbed over 6%. Strategy, the largest corporate bitcoin holder, was up 7%. Bitcoin itself ground higher, hitting session highs near $81,500.

"For too long, regulatory uncertainty has sent talent, investment, and innovation overseas, strengthening foreign competitors while leaving American builders without the certainty they need to compete," said Blockchain Association CEO Summer Mersinger, who called the committee vote a "defining moment." Ripple CEO Brad Garlinghouse was blunter: "If the largest economy in the world is going to lead on crypto, and it must, this is the moment."

Still Some Runway Ahead

Thursday's vote was a milestone, but it is not the finish line. The bill still needs to be reconciled with a separate version approved by the Senate Agriculture Committee, and the full Senate will require 60 votes to pass it, meaning a significant number of Democrats will have to come on board. The House passed its own version of the legislation last year, so the two chambers will also need to hammer out a unified text before anything heads to President Trump's desk.

The largest outstanding issue is an ethics provision intended to limit government officials, including the president, from profiting off crypto. Democrats have made clear they will not move forward without some version of it, while White House crypto adviser Patrick Witt has said the administration will not tolerate language targeting a specific officeholder. Both sides appeared at least open to finding common ground, with Cody Carbone of the Digital Chamber telling reporters that a deal on the ethics provision is likely a prerequisite for getting the bill to a floor vote at all. The window, several lawmakers noted, is probably August.

A Framework Built to Last

What makes the Clarity Act different from the patchwork of guidance and enforcement actions that have defined crypto policy for the past decade is its ambition. It does not try to pigeonhole digital assets into frameworks designed for equities or futures contracts decades ago. It builds something new, with defined registration pathways for digital commodity exchanges, brokers, and dealers, as well as clear definitions covering blockchain applications, protocols, and smart contracts.

Ji Hun Kim, CEO of the Crypto Council for Innovation, put it plainly after the vote: "Clear durable rules will help drive greater institutional and retail adoption, support innovation, create more high quality jobs in the U.S., protect Americans, and ensure that our country leads when it comes to digital assets policy and innovation."

The GENIUS Act, which passed the full Senate 68-30 last year, showed that comprehensive crypto legislation can attract broad support once the details are sorted. The Clarity Act is a harder lift, covering more ground and touching more competing interests. But Thursday's committee vote suggests the political will is there, and the industry is watching closely.

"Durable, lasting digital asset policy must be built on a bipartisan foundation," Mersinger added. By that measure, the Clarity Act is not finished yet. But for the first time in a long while, it looks like it might actually get there.

Why This Matters for the Future of Digital Assets

Let's be clear about all of this: Thursday was a great day for anyone who believes that digital assets have a meaningful role to play in the future of finance. I am certainly one of those. Not because the Clarity Act is perfect, and not because it's done, but because it signals something important that has been missing for years: the U.S. government is starting to treat this industry like it's here to stay.

The case for optimism goes beyond this single vote. The GENIUS Act passing 68-30 last year proved that stablecoin legislation could attract real bipartisan support. Institutional investment in Bitcoin ETFs has steadily matured. Major financial players who once dismissed crypto as a fringe asset are now building infrastructure around it. The underlying technology, particularly in DeFi and tokenization, keeps advancing regardless of what Washington does. What regulation does is create the conditions for all of that to compound. It clears the path for pension funds, endowments, and large asset managers who have been sitting on the sidelines waiting for legal certainty before committing serious capital.

That said, the Senate still has to close the deal, and that is not a given. The remaining sticking points on the ethics provision and law enforcement concerns are real, not just noise. Lawmakers like Senator Kirsten Gillibrand have been consistent that they will not deliver Democratic votes without meaningful conflict-of-interest guardrails, and that is a fair position. The 60-vote threshold means the bill needs to be genuinely bipartisan, not just technically so.

On timing, the realistic window is narrower than it might appear. Industry insiders, including Cody Carbone of the Digital Chamber, have pointed to August as a likely deadline if the bill is to move this year. Congress typically slows through the fall ahead of elections, and the legislative calendar fills up fast. That gives negotiators roughly ten to twelve weeks to reconcile the two committee versions, finalize the ethics language, and lock down the 60 votes needed for a floor vote. It is achievable, but it requires both parties to decide they want a deal more than they want a talking point.

If it does pass, the long-term impact will be substantial. Clear rules attract capital. Capital attracts builders. Builders create products that bring in users. That cycle, running inside a legitimate regulatory framework and anchored in the world's largest economy, is how digital assets stop being a niche and become infrastructure. You know...that "mass adoption" that people have been talking about for years? Well, this could be it. It might not look like how we all imagined, but what ever really does? Thursday was one huge step in that direction. The Senate now needs to finish what it started and we need to come together to make sure they all know that they need to do just that. Let's get it done.

Florida Passes First State-Level Stablecoin Bill in U.S.

Florida lawmakers have cleared Senate Bill 314 (SB-314), a state-level stablecoin bill, with final approval now pending from the governor.

In a recent post on X, Samuel Armes, founder of the Florida Blockchain Association, said the Florida Senate had cleared Senate Bill 314 with a unanimous 37–0 vote. With this clearance, the bill now awaits final approval from Governor Ron DeSantis.

According to Armes, “the bill has now passed the Senate and the House and will be signed by DeSantis within the next 30 days.” Once signed by DeSantis, SB-314 will become law.

What is the Senate Bill (SB-314)?

Introduced by Senator Bryan Burton on October 31, 2025, Senate Bill 314 (SB 314) creates a state regulatory framework for companies issuing stablecoins in Florida.

SB 314 was introduced to ensure clarity in how stablecoins are issued amid ongoing regulatory disparities, particularly at the state level.

By approving SB 314, the Florida Legislature aims to:

1. Provide regulatory clarity for crypto businesses operating in the state.

2. Prevent fraud and financial instability. The bill requires stablecoin issuers to hold actual reserves, protecting users’ funds.

3. Position Florida as a crypto-friendly hub, attracting both blockchain and fintech companies.

If SB-314 eventually gets signed into law, stablecoin companies would need Florida’s licensing and approval before they can operate.

And to get licensed, these companies would need to show proof of 1:1 reserves backing their stablecoins, have their reserves independently audited, and maintain clear redemption policies that allow users to convert stablecoins to dollars.

Remember the TerraUSD collapse, one of the largest stablecoin failures in 2022, which resulted in losses exceeding $40 billion after the UST coin lost its dollar peg? The SB-314 bill aims to prevent similar events by requiring stablecoin issuers to have their reserves regularly audited.

The State of Crypto in Florida

Unlike some U.S. states that have imposed strict anti-crypto policies, Florida has positioned itself as one of the most crypto-friendly.

In January 2023, the Florida Senate amended the state's Money Services Business (MSB) law to include virtual currency, defining it at the state level and reducing regulatory ambiguity for crypto businesses.

In October 2025, the Florida Senate filed House Bill 183, concerning crypto investment authority, and House Bill 175, aimed at stablecoin registration flexibility. If signed into law, the bills would allow Florida’s Chief Financial Officer to allocate up to 10% of certain state funds into Bitcoin and other digital assets, while also easing compliance requirements for stablecoin issuers.

Banks Are Drawing a Hard Line on Stablecoin Yield

Washington has spent the past several months talking about crypto clarity. What it got this week was something closer to a standoff.

At the center of the latest White House meeting between crypto executives and banking lobbyists was a surprisingly narrow issue that has turned into a major fault line: stablecoin yield.

On paper, the CLARITY Act is supposed to settle jurisdictional turf wars between regulators and create a workable framework for digital assets in the United States. In practice, negotiations have slowed to a crawl over whether stablecoin holders should be allowed to earn rewards.

Crypto companies came to the table expecting to negotiate. Bank representatives arrived with something closer to a red line.

The Yield Problem

Stablecoin yield sounds simple. Platforms offer incentives, rewards, or returns to users who hold dollar-backed tokens. Sometimes that comes from lending activity. Sometimes it comes from promotional programs. Structurally, it does not always look like a bank deposit.

Banks are not buying that distinction.

From their perspective, if consumers can hold tokenized dollars and earn a return without stepping inside the banking system, that looks a lot like deposit competition. And not just competition, but competition without the same regulatory burden.

Banks operate under capital requirements, liquidity ratios, deposit insurance rules, stress testing frameworks, and layers of federal oversight. Stablecoin issuers, even under proposed legislation, would not be subject to the same regime.

So the banking lobby’s position has been blunt. No yield. Not from issuers, not indirectly through affiliated programs, not in ways that replicate interest-bearing accounts.

The crypto side sees that as overreach.

Is This About Risk or About Control?

Publicly, banks frame their opposition as a financial stability issue. If large amounts of capital flow out of insured deposits and into stablecoins offering yield, that could shrink the deposit base that supports lending. In a stress scenario, they argue, the dynamic could amplify volatility.

There is logic there. Deposits are the backbone of bank balance sheets. Disintermediation is not a trivial concern.

But crypto executives are asking a quieter question. If the issue is really about safety, why push for a blanket prohibition rather than tighter guardrails? Why not cap yield structures, restrict how they are funded, or impose disclosure standards?

Why eliminate them entirely?

Some in the industry suspect the answer is competitive pressure. Stablecoins have already become critical plumbing for crypto markets, facilitating trading, settlement, and cross-border transfers. Add yield into the equation and they start to look even more like digital savings instruments.

That begins to encroach on traditional banking territory.

The Competitive Threat

Banks have historically tolerated crypto in its speculative corners. Trading tokens is volatile, niche, and largely outside the core consumer banking relationship.

Stablecoins are different. They are dollar-denominated. They are increasingly integrated into payment systems. They can move across borders faster than traditional rails. And they are programmable.

Now imagine those same tokens offering yield, even modest incentives. The psychological shift for consumers could be meaningful. Why leave idle cash in a checking account earning almost nothing if a tokenized version offers some return and similar liquidity?

To bankers, that is not innovation. That is deposit leakage.

And in a higher rate environment, where funding costs matter, deposit competition becomes more acute.

The Legislative Bottleneck

The CLARITY Act was supposed to resolve long-running disputes between regulators and provide certainty for digital asset firms operating in the United States. Instead, stablecoin yield has turned into the sticking point holding up broader progress.

White House officials have reportedly pressed both sides to find compromise language. So far, that compromise remains elusive.

Crypto firms argue that banning yield outright could push innovation offshore. Jurisdictions in Asia and parts of Europe are moving ahead with stablecoin frameworks that do not automatically prohibit reward structures. The fear in Washington’s crypto circles is that overcorrection could hollow out domestic competitiveness.

Banking groups counter that allowing yield would create a parallel banking system without equivalent safeguards.

The tension is not just technical. It is philosophical.

A Larger Question About Money

At its core, this debate is about who gets to intermediate digital dollars.

If stablecoins become widely used and allowed to offer returns, they could evolve beyond trading tools into mainstream financial instruments. That challenges the traditional hierarchy where banks sit at the center of deposit-taking and credit creation.

Banks are not opposed to digital dollars in theory. Many are experimenting with tokenization and blockchain infrastructure themselves. But they want those innovations inside the regulated banking perimeter, not outside of it.

Crypto companies, on the other hand, see decentralization and alternative rails as the point.

So when banks push to ban stablecoin yield entirely, the crypto industry reads it as more than prudence. It looks like an attempt to protect market share.

The Bottom Line

For now, negotiations continue. There is still political appetite in Washington to pass comprehensive crypto legislation, especially as digital asset markets remain a significant part of the financial system.

But unless lawmakers can thread the needle between stability concerns and competitive fairness, stablecoin yield could remain the issue that stalls everything else.

And that leaves an uncomfortable reality.

If the United States cannot decide whether digital dollars are allowed to earn a return, the market may decide elsewhere.

Coinbase Breaks With Senate on Crypto Bill as Stablecoin Rules Spark Pushback

Coinbase Draws a Line in the Sand on Market Structure Bill

Coinbase is stepping back from Washington’s biggest crypto push yet.

Just days before a crucial vote in the Senate Banking Committee, the largest US crypto exchange says it will not support the Senate’s sweeping crypto market structure bill in its current form. The message from Coinbase CEO, Brian Armstrong, is blunt. Regulatory clarity matters, but not at any cost.

The move highlights a growing divide between lawmakers eager to lock in federal rules and an industry increasingly wary of legislation that could reshape its business in unintended ways.

A Bill Meant to End the Gray Area

The Senate bill, months in the making, is designed to finally spell out how digital assets are regulated in the United States. At its core, the proposal tries to answer long-standing questions about which crypto assets fall under securities law, which should be treated as commodities, and how oversight should be split between regulators.

For years, crypto companies have complained that the lack of clear rules has pushed innovation offshore and left firms vulnerable to enforcement actions after the fact. On paper, this bill is supposed to fix that.

But as the text has taken shape, it has also picked up provisions that some in the industry see as deal-breakers.

Stablecoin Rewards Become the Flashpoint

For Coinbase, the biggest problem sits with stablecoins.

The draft legislation includes language that could sharply limit or effectively eliminate rewards paid to users who hold stablecoins on platforms like Coinbase. These rewards are not technically interest paid by issuers, but incentives offered by exchanges and intermediaries. Still, critics argue they look and feel a lot like bank deposits, without bank-style regulation.

Traditional banking groups have pushed hard for tighter rules here. Their concern is straightforward. If consumers can earn yield on dollar-pegged crypto tokens outside the banking system, deposits could drain from insured banks, particularly smaller ones.

Coinbase sees it differently. Stablecoin rewards have become a meaningful part of how crypto platforms compete and how users engage with dollar-based crypto products. Cutting them off, the company argues, would harm consumers and hand an advantage back to traditional finance.

In private and public conversations, Coinbase executives have made it clear that they are unwilling to back a bill that undercuts what they view as a legitimate and already regulated product.

"After reviewing the Senate Banking draft text over the last 48 hours, Coinbase unfortunately can’t support the bill as written,” Armstrong said. "This version would be materially worse than the current status quo, we'd rather have no bill than a bad bill."

Why This Matters Beyond Coinbase

Coinbase’s stance carries weight. It is one of the most politically active crypto companies in Washington and often serves as a bellwether for broader industry sentiment.

If Coinbase is out, others may quietly follow.

That raises the risk that lawmakers end up with a bill that lacks meaningful industry buy-in, or worse, one that passes but leaves key players unhappy enough to challenge or work around it.

Some firms are already exploring alternatives, including banking charters or trust licenses, as a hedge against restrictive federal rules. Others may simply slow US expansion and look overseas.

A Narrow Path Forward in the Senate

The timing is not ideal.

The Senate Banking Committee is expected to vote on the bill imminently, but support remains fragile. Lawmakers are divided not just on stablecoins, but also on how to handle decentralized finance, custody rules, and even ethics provisions tied to political exposure to crypto.

Add in election-year politics, and the window for compromise looks tight.

If the bill stalls or fails in committee, there is a real chance it gets pushed into the next Congress. That would mean at least another year, and likely more, of regulatory uncertainty.

No Law vs a Bad Law

Behind the scenes, a familiar argument is playing out.

Some in Washington believe that imperfect legislation is better than none at all. The industry, scarred by years of enforcement-first regulation, is no longer convinced.

Coinbase’s decision reflects a growing view among crypto companies that a flawed law could do more long-term damage than continued ambiguity. Once rules are written into statute, they are far harder to undo.

For now, the standoff continues.

Whether lawmakers soften the bill to keep major players on board or push ahead regardless may determine not just the fate of this legislation, but the shape of US crypto regulation for years to come.

Stay Connected

You can stay up to date on all News, Events, and Marketing of Rare Network, including Rare Evo: America’s Premier Blockchain Conference, happening July 28th-31st, 2026 at The ARIA Resort & Casino, by following our socials on X, LinkedIn, and YouTube.