#Blockchain Policy

Minnesota Approves Crypto Custody Services for Banks

Minnesota has enacted a law that allows banks and credit unions in the state to offer cryptocurrency custody services, with the law expected to take effect on Aug. 1, 2026.

The bill, HF 3709, was signed into law on Friday by Minnesota state governor Tim Walz, with the state legislature’s website stating that cryptocurrency custody services may now be offered and performed in the state.

While this is a significant milestone for crypto adoption in the state, the law also requires banks and credit unions interested in offering crypto custody services to submit a written notice detailing their risk management frameworks to the Minnesota Commissioner of Commerce at least 60 days before commencing such services.

The Minnesota Commissioner of Commerce will serve as the primary regulator, overseeing crypto custody services offered by banks and credit unions in the state.

Banks and credit unions interested in offering crypto custody services are also required to maintain a comprehensive written policy covering their internal controls, security, risk management, and compliance frameworks, while also segregating their clients’ assets from institutionally owned assets.

According to Representative Bernie Perryman, one of the primary sponsors of HF 3709, the legislation aims to establish a trustworthy framework that enables financial institutions to work with and safeguard Minnesotans' crypto assets, especially as crypto becomes more mainstream.

“House File 3709 is about ensuring that Minnesota-based financial institutions are allowed to evolve alongside their customers and members rather than forcing Minnesotans to rely on unregulated, out-of-state or offshore providers for services that are already in use today,” Perryman said in a March press release.

The passage of HF 3709 comes just a few weeks after the Minnesota governor banned the use and ownership of crypto kiosks and ATMs across the state, citing their growing use in fraud.

With the passage of this bill, Minnesota now joins Wyoming, New York, and Virginia, which have passed similar bills that allow banks and credit unions to offer crypto custody services.

Florida Passes First State-Level Stablecoin Bill in U.S.

Florida lawmakers have cleared Senate Bill 314 (SB-314), a state-level stablecoin bill, with final approval now pending from the governor.

In a recent post on X, Samuel Armes, founder of the Florida Blockchain Association, said the Florida Senate had cleared Senate Bill 314 with a unanimous 37–0 vote. With this clearance, the bill now awaits final approval from Governor Ron DeSantis.

According to Armes, “the bill has now passed the Senate and the House and will be signed by DeSantis within the next 30 days.” Once signed by DeSantis, SB-314 will become law.

What is the Senate Bill (SB-314)?

Introduced by Senator Bryan Burton on October 31, 2025, Senate Bill 314 (SB 314) creates a state regulatory framework for companies issuing stablecoins in Florida.

SB 314 was introduced to ensure clarity in how stablecoins are issued amid ongoing regulatory disparities, particularly at the state level.

By approving SB 314, the Florida Legislature aims to:

1. Provide regulatory clarity for crypto businesses operating in the state.

2. Prevent fraud and financial instability. The bill requires stablecoin issuers to hold actual reserves, protecting users’ funds.

3. Position Florida as a crypto-friendly hub, attracting both blockchain and fintech companies.

If SB-314 eventually gets signed into law, stablecoin companies would need Florida’s licensing and approval before they can operate.

And to get licensed, these companies would need to show proof of 1:1 reserves backing their stablecoins, have their reserves independently audited, and maintain clear redemption policies that allow users to convert stablecoins to dollars.

Remember the TerraUSD collapse, one of the largest stablecoin failures in 2022, which resulted in losses exceeding $40 billion after the UST coin lost its dollar peg? The SB-314 bill aims to prevent similar events by requiring stablecoin issuers to have their reserves regularly audited.

The State of Crypto in Florida

Unlike some U.S. states that have imposed strict anti-crypto policies, Florida has positioned itself as one of the most crypto-friendly.

In January 2023, the Florida Senate amended the state's Money Services Business (MSB) law to include virtual currency, defining it at the state level and reducing regulatory ambiguity for crypto businesses.

In October 2025, the Florida Senate filed House Bill 183, concerning crypto investment authority, and House Bill 175, aimed at stablecoin registration flexibility. If signed into law, the bills would allow Florida’s Chief Financial Officer to allocate up to 10% of certain state funds into Bitcoin and other digital assets, while also easing compliance requirements for stablecoin issuers.

Florida Lawmakers Renew Push for State Bitcoin Reserve

Florida lawmakers are once again taking up the question of whether the state should hold Bitcoin as part of its long-term financial strategy, reviving a proposal that failed to advance last year but now returns with a revised structure and new momentum.

The effort comes as crypto markets have stabilized after a volatile stretch, with Bitcoin regaining ground and institutional interest continuing to grow. Against that backdrop, Florida’s move places it back into a widening national debate over whether digital assets belong on government balance sheets.

At the center of the push is House Bill 1039, filed during the 2026 legislative session, which would establish a Florida Strategic Cryptocurrency Reserve.

What the Bill Would Do

House Bill 1039 proposes creating a standalone reserve fund held outside the State Treasury and overseen by Florida’s Chief Financial Officer. The CFO would be granted authority to acquire, hold, sell, or manage digital assets under prudent investment standards, including the ability to contract with third-party custodians and service providers.

While the bill is written broadly, it sets strict eligibility rules for any asset included in the reserve. To qualify, a cryptocurrency must have maintained an average market capitalization of at least $500 billion over the prior two years. Based on current market conditions, that threshold effectively limits the reserve to Bitcoin.

The legislation also establishes a Strategic Cryptocurrency Reserve Advisory Committee, designed to provide guidance and oversight. At least three members would be required to have direct experience investing in digital assets, acknowledging the technical and operational complexity involved in managing crypto at the state level.

If passed, the bill would take effect on July 1, 2026.

A Return to an Unfinished Debate

Florida’s renewed push follows the collapse of similar efforts during the 2025 legislative session. Those earlier proposals would have allowed the state to allocate up to 10 percent of certain public funds directly into Bitcoin but were ultimately withdrawn before a final vote.

Another bill introduced around the same time would have gone even further, authorizing the CFO and the State Board of Administration to invest portions of public and pension funds into Bitcoin, crypto exchange-traded products, tokenized securities, and non-fungible tokens. That proposal included detailed custody and compliance provisions but also failed to gain enough traction to advance.

This year’s bill reflects a more cautious approach. By placing the reserve outside the main treasury and narrowing eligible assets, lawmakers appear to be trying to strike a balance between experimentation and risk control.

Market Context and State Competition

The timing of Florida’s move is notable. Bitcoin prices have rebounded from earlier lows, and digital assets are increasingly being discussed in the context of long-term portfolio diversification rather than short-term speculation. Exchange-traded products, corporate treasury allocations, and broader institutional adoption have shifted how policymakers frame the asset.

Florida is not alone. Texas moved ahead last year with legislation establishing a state-managed Bitcoin reserve funded with public dollars, making it the most aggressive example so far of a U.S. state embracing Bitcoin at an institutional level. Other states, including Arizona and New Hampshire, have passed narrower frameworks that stop short of direct funding.

Many similar proposals across the country have stalled, underscoring how politically sensitive the issue remains.

Supporters and Skeptics Remain Split

Supporters of Florida’s proposal argue that a Bitcoin reserve could help diversify state assets, hedge against inflation, and position Florida as a forward-looking financial hub. They also point to the advisory committee and high eligibility threshold as safeguards against reckless exposure.

Critics continue to raise concerns about volatility, custody risks, and the appropriateness of using public funds for an asset that can swing sharply in value. Questions about accounting standards, security practices, and public accountability are expected to feature prominently as the bill moves through committee hearings.

What Happens Next

House Bill 1039 must clear multiple legislative hurdles, including committee review, passage in both chambers, and approval by the governor. While its future remains uncertain, the proposal signals that Florida lawmakers are not ready to abandon the idea of state-level crypto reserves.

As more governments revisit Bitcoin through a policy lens rather than a speculative one, Florida’s debate could offer a clearer picture of how digital assets fit into the next phase of public finance.

Stay Connected

You can stay up to date on all News, Events, and Marketing of Rare Network, including Rare Evo: America’s Premier Blockchain Conference, happening July 28th-31st, 2026 at The ARIA Resort & Casino, by following our socials on X, LinkedIn, and YouTube.

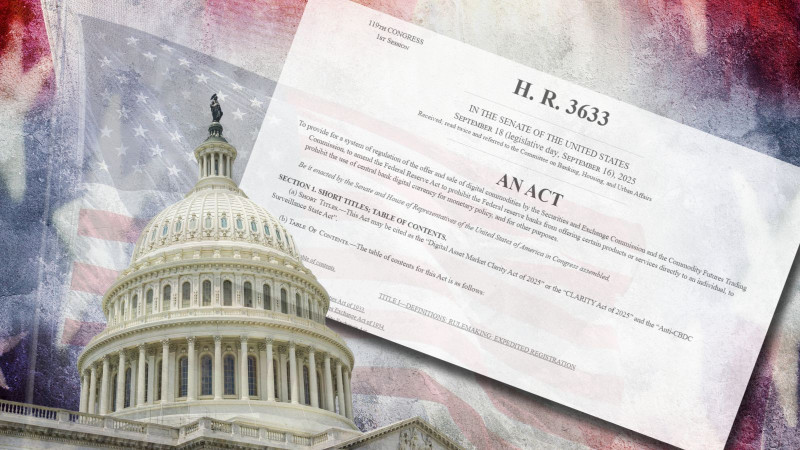

What the CLARITY Act Means for Crypto and Why It Matters So Much

If you have spent any real time building, trading, or working in crypto in the U.S., you already know the pattern. The rules are never fully clear. Guidance usually comes after the fact. And “compliance” often feels less like a checklist and more like a guessing game.

That is the environment the Digital Asset Market Clarity Act, better known as the CLARITY Act, is trying to change.

On January 15, 2026, the Senate Banking Committee is scheduled to hold a critical markup session on the bill. That might sound like inside-baseball legislative procedure, but it is not. A markup is where lawmakers decide what a bill really is. Language gets tightened. Loopholes get closed or widened. Entire sections can disappear.

For crypto, this is one of those moments where the future shape of U.S. regulation is actually being decided.

The problem CLARITY is trying to solve

Right now, crypto regulation in the U.S. is reactive.

The laws that exist were written long before blockchains, tokens, or decentralized networks. Regulators have mostly tried to force crypto into frameworks that were never designed for it, often relying on enforcement actions to define the rules retroactively.

CLARITY is an attempt to stop doing that.

The bill starts from a simple premise: not everything in crypto is the same, so it should not all be regulated the same way.

Launching a token to fund a network is not the same as trading that token years later. Writing open-source code is not the same as holding customer funds. Running a wallet is not the same as running an exchange.

Those distinctions sound obvious inside the industry. CLARITY tries to make them explicit in law.

Tokens are not frozen in time

One of the most important ideas in the bill is that a token’s legal treatment should not be locked forever to how it was first sold.

Under the current system, if a token was ever distributed in a way that looks like fundraising, it can carry securities risk indefinitely. Even if the network decentralizes. Even if the original team steps away. Even if the token functions more like a commodity than an investment.

CLARITY tries to separate:

-

The initial transaction, which may look like an investment contract

-

The token itself, once it is broadly distributed and actively used

That distinction matters because it opens the door to secondary markets operating without constant legal uncertainty, while still keeping guardrails around early fundraising.

What “mature blockchain” actually means

To make that transition possible, CLARITY introduces the concept of a mature blockchain system.

Stripped of legal language, the question is pretty straightforward: does anyone actually control this thing?

If a small group can still unilaterally change the rules, supply, or governance, regulators get more leverage. If control is meaningfully distributed and no one actor is calling the shots, the regulatory burden can ease.

The bill creates a certification process around this idea, with a defined window for regulators to challenge a claim of maturity.

This is one of the most debated sections of the bill. It is also one of the most important. The standard has to be real, but it also has to be achievable. Senate changes here could dramatically affect how useful the bill ends up being.

How token launches could work going forward

CLARITY does not remove oversight from token launches. Instead, it tries to make that oversight fit reality.

The bill allows certain token offerings to proceed under an exemption, but only with meaningful disclosures. Projects would need to explain things like:

-

How token supply and issuance work

-

What rights, if any, token holders have

-

How governance actually functions in practice

-

What the project plans to build and what risks exist

The shift here is away from clever legal gymnastics and toward plain-English transparency. For founders, that could mean fewer surprises and a clearer sense of what is expected.

Why exchanges are watching this so closely

For U.S. crypto exchanges, CLARITY is largely about secondary markets.

Today, listing a token can feel risky even if that same asset trades freely outside the U.S. The legal line between primary fundraising and secondary trading has never been cleanly drawn.

CLARITY tries to draw that line. If it holds, exchanges would finally have a framework designed specifically for spot crypto markets, instead of trying to fit into rules written for something else.

A bigger role for the CFTC

Another major shift is regulatory jurisdiction.

CLARITY gives the CFTC clear authority over spot markets for digital commodities, not just derivatives. It also creates new registration paths for exchanges, brokers, and dealers that are tailored to how crypto markets actually function.

Importantly, the bill pushes for speed. It directs the CFTC to create an expedited registration process, acknowledging that waiting years for clarity is not realistic in fast-moving markets.

DeFi, software, and where things get tricky

DeFi is where the bill walks a tightrope.

CLARITY says that people should not be treated as regulated intermediaries just for building or maintaining software, running nodes, providing wallets, or supporting non custodial infrastructure. It also makes clear that participating in certain liquidity pools, by itself, should not automatically trigger exchange-level regulation.

At the same time, fraud and manipulation laws still apply.

Supporters see this as long overdue recognition that infrastructure is not the same as custody or brokerage. Critics worry about edge cases, especially where front ends, admin controls, or governance tokens blur the lines.

This is an area where Senate edits could have outsized impact.

Federal rules versus state rules

The bill also leans toward stronger federal oversight and narrower state-by-state requirements in certain areas.

For companies, that means fewer conflicting regimes and lower compliance friction. For critics, it raises concerns about losing fast-moving state enforcement in an industry that still sees its share of bad actors.

That tension is not going away, and it will likely surface again during markup.

Self custody, explicitly protected

One of the clearest statements in CLARITY is its protection of self custody.

The bill explicitly affirms the right to hold your own crypto and transact peer to peer for lawful purposes. In an environment where indirect restrictions have been a constant fear, putting this into statute is not symbolic. It is structural.

Developers get some breathing room

CLARITY also addresses a long-running concern among builders.

The bill says that non-controlling developers and infrastructure providers should not be treated as money transmitters simply for writing code or publishing software, as long as they do not control user funds or transactions.

For many developers, this removes a quiet but persistent legal cloud that has hung over the industry.

Why January 15 is such a big deal

The January 15 markup is where all of this either becomes real or starts to unravel.

This is where lawmakers decide how strict the maturity standards are, how wide the DeFi exclusions go, how much authority regulators actually get, and whether the bill delivers usable clarity or just new gray areas.

If CLARITY moves forward in a recognizable form, it becomes the most serious attempt yet to give crypto a durable U.S. market structure. If it does not, the industry likely stays where it is now, building first and hoping the rules catch up later.

How you can get involved?

This is also the moment where voices outside Washington still matter.

Lawmakers are actively weighing feedback. Staffers are reading messages. Offices are tracking where their constituents stand. Silence gets interpreted as indifference, and indifference makes it easier for complex bills to stall or be watered down.

If you believe crypto should have clear rules instead of enforcement-by-surprise, this is the time to say so.

That means contacting your representatives. Find out who your representative is and where they stand on crypto policy. Tell them that market structure clarity matters. Explain why builders, users, and businesses need predictable rules to stay in the U.S. Explain why self custody, open infrastructure, and lawful innovation should be protected, not pushed offshore.

It also means supporting organizations that are trying to organize that voice.

One such organization is Rare PAC, a political action committee advocating for regulatory clarity, innovation, and economic opportunity powered by decentralized technologies. Rare PAC works to ensure that the United States remains a global leader in those decentralized technologies and supports candidates who are committed to building A Crypto Forward America.

Bills like CLARITY do not pass or fail in a vacuum. They pass because people show up, speak up, and make it clear that getting this right matters.

January 15 is not the end of the process, but it is one of the moments that will shape everything that comes after.

Trump Appoints Pro-Crypto Lawyer Michael Selig to Lead the CFTC

Trump Appoints Pro-Crypto Lawyer Michael Selig to Lead the CFTC

A new chapter for U.S. crypto regulation

President Donald Trump has nominated Michael Selig to serve as Chair of the U.S. Commodity Futures Trading Commission (CFTC). The move marks one of the clearest signals yet that the administration intends to take a pro-innovation approach toward digital assets.

If confirmed by the Senate, Selig would succeed acting Chair Caroline Pham and lead one of the key federal agencies overseeing U.S. derivatives and crypto markets. His background in crypto policy and law positions him as a potential bridge between the CFTC and the Securities and Exchange Commission (SEC), which have often clashed over digital asset oversight.

Who is Michael Selig

Michael Selig currently serves as Chief Counsel for the SEC’s Crypto Task Force, where he has played a central role in shaping digital asset policy. Before joining the SEC, Selig worked at the law firm Willkie Farr & Gallagher, focusing on fintech and blockchain regulation. Earlier in his career, he interned at the CFTC, giving him firsthand insight into how the agency functions.

Throughout his career, Selig has been recognized for his deep understanding of both traditional finance and emerging crypto ecosystems. He is considered one of the few U.S. legal experts who can navigate the complex line between securities and commodities law as it applies to digital assets.

Why This Matters

The appointment sends a strong signal that the administration aims to modernize U.S. financial regulation. Selig is known for supporting clear, innovation-friendly frameworks rather than strict enforcement-first approaches.

For years, crypto companies and investors have criticized U.S. regulators for sending mixed messages about what counts as a security versus a commodity. The result has been uncertainty that stifled innovation and pushed some firms overseas. With Selig at the helm, the CFTC may seek to provide clarity while fostering responsible growth in digital markets.

The nomination also reflects a broader shift in Washington. Rather than treating digital assets purely as a threat, policymakers appear to be viewing blockchain technology as an opportunity for U.S. leadership in global finance.

What to Watch

The next step for Selig will be Senate confirmation, a process that could include tough questioning about his crypto-friendly stance. Lawmakers are divided on how much authority the CFTC should have over digital assets, and Selig’s confirmation could become a flashpoint in the broader debate over crypto regulation.

If approved, his leadership could influence key policy areas, including:

-

CFTC-SEC Coordination: Efforts to align rules between the two agencies and reduce regulatory overlap.

-

Market Structure Reform: Defining how tokens, stablecoins, and decentralized finance products are classified.

-

Industry Engagement: Building formal channels for dialogue between regulators and blockchain innovators.

-

Global Competitiveness: Positioning the U.S. as a leading market for compliant digital asset innovation.

The Bigger Picture

Selig’s nomination comes at a pivotal time for crypto policy. Congress is considering new legislation that could expand or clarify the CFTC’s jurisdiction over digital assets. Having a chair who understands both the technology and the law could make a major difference in how those rules are implemented.

The crypto industry has responded positively, viewing Selig as someone who can combine pragmatic regulation with a commitment to innovation. However, optimism is tempered by the reality that new leadership alone will not resolve all challenges. Effective reform will still require interagency cooperation, clear legislative backing, and strong consumer protections.

Final Thoughts

Michael Selig’s appointment represents more than just a personnel change. It could mark the start of a new era for U.S. crypto policy, where innovation and regulation are not seen as opposing forces.

If confirmed, Selig will face the challenge of turning a fragmented regulatory landscape into one that encourages growth while maintaining market integrity. His success will depend on balancing ambition with accountability, and on ensuring that the U.S. remains both competitive and credible in the global digital economy.