#Solana

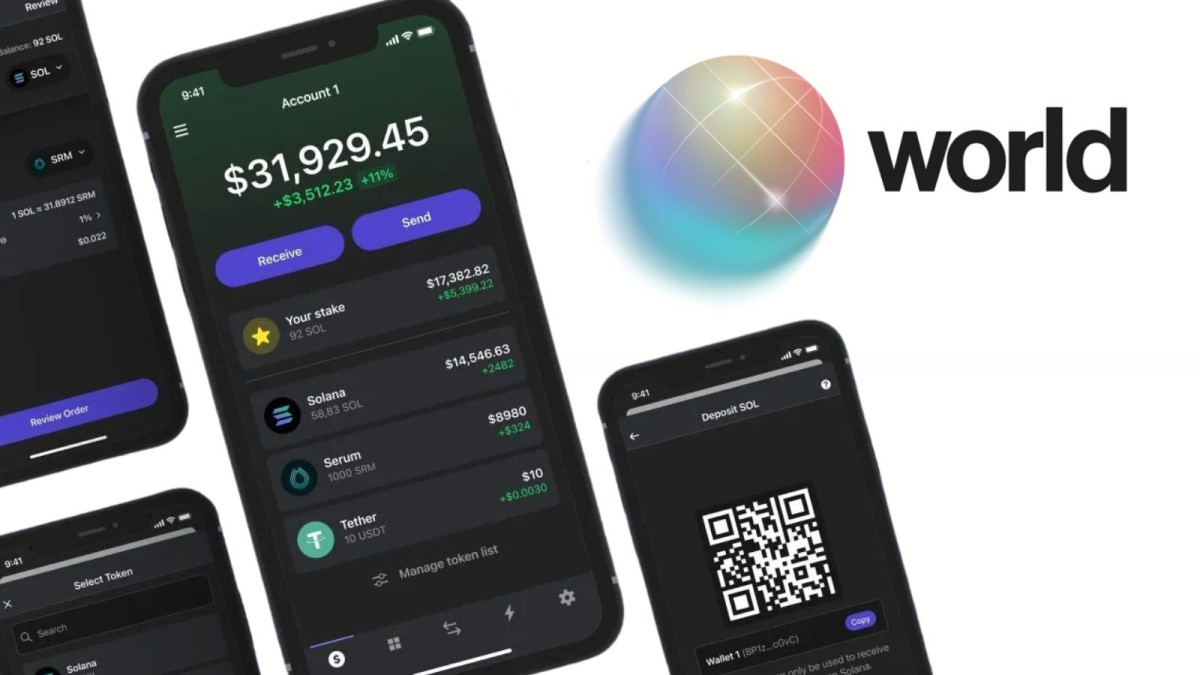

World Prediction Market Launches in Phantom Wallet

World, a fully on-chain, Solana native prediction market powered by Chainlink that aims to compete with Kalshi and Polymarket, has launched on Phantom Wallet.

Image credit: x.com

According to the team, the World prediction market will allow users to predict outcomes on crypto price movements and the ongoing 2026 FIFA Men's World Cup. Additional markets across sports, geopolitics, and macroeconomics will be added in the coming weeks.

"Prediction markets are one of the most powerful applications you can build on a high-performance blockchain," said Pedro Miranda, Head of Consumer at the Solana Foundation. "World is designed to show what Solana makes possible: real-time markets, on-chain settlement, and a user experience that meets people where they are."

Unlike most prediction markets that require users to interact with centralized infrastructure, World is designed to operate entirely on-chain. Every market, every position, and every settlement happens on-chain; as such, users do not have to move their funds to any custodial or centralized entity, as they can interact directly with Solana liquidity.

The platform uses $CASH as its settlement stablecoin. Since it’s launched directly within the Phantom Wallet, World will be available to more than 20 million Phantom Wallet users. It is also important to note that this World project is entirely different from Sam Altman's World. This World is a prediction market project, while Sam Altman's World is an identity project.

World's launch comes at a time when prediction markets are gaining significant traction, especially since the start of the 2026 FIFA Men's World Cup. Since early June, prediction market platforms, including Kalshi and Polymarket, have seen inflows of more than $3.8 billion.

Despite regulatory challenges in some jurisdictions, prediction market companies continue to grow and expand. Kalshi and Polymarket have both recently secured substantial funding from investors. Kalshi recently raised funding at a $22 billion valuation, while Polymarket raised $600 million at a $15 billion valuation and is reportedly in talks to raise an additional $400 million.

Exodus Partners With Ondo To Launch Tokenized Stocks

Exodus Movement Inc. (NYSE American: EXOD), a publicly traded financial technology company and developer of the Exodus wallet, has partnered with Ondo Finance to launch Exodus Markets, a platform for trading tokenized assets.

With Exodus Markets, users can now buy and sell more than 200 tokenized stocks, exchange-traded funds (ETFs), and real-world assets directly in the Exodus wallet app on the Solana blockchain.

"Tokenized stocks are one of the most important developments in modern finance," said JP Richardson, CEO and co-founder of Exodus.

"For the first time, our customers can trade and hold tokenized equities with the same direct control and global access they expect from crypto. Exodus is becoming the front door to every asset you hold, without compromising on trust and control."

The launch of Exodus Markets aligns with Exodus’s goal of transforming from a custodial wallet into a full financial platform that allows users to trade, earn rewards, send, spend, and manage money.

As part of its efforts to become a comprehensive financial app, Exodus launched Exodus Pay, a self-custodial payment feature within the Exodus app that enables users to transact with digital assets, including stablecoins, for everyday purchases. The company also launched XO Cash, a stablecoin pegged to the U.S. dollar.

The Tokenization Space

The tokenization space, particularly real-world assets (RWAs), has experienced significant growth over the past 1 to 2 years. Excluding stablecoins, the tokenization sector grew from roughly $5 billion to $6 billion at the start of 2025 to $27 billion to $31 billion or more by mid 2026, representing an increase of more than 400% over a period of 15 to 18 months.

Several institutions are also entering this growing sector, with Bitget most recently launching Reality, its real-world asset (RWA) platform. Kraken has also launched xChange, an on-chain trading engine designed for trading tokenized equities. MetaMask, Trust Wallet, Blockchain.com, and Robinhood have also made strategic moves to enter the sector, partnering with RWA firms and rolling out tokenized assets and stocks.

Given the level of growth and adoption the real-world asset and tokenization sector has seen so far, several projections have been made regarding its future potential. The Boston Consulting Group and Ripple have projected that the sector could be worth more than $15 trillion by 2030.

Solayer Launches Margin Trade Mainnet for Multi-Asset Perpetual Trading

Solayer, a hardware-accelerated Layer 1 blockchain and Solana’s first restaking platform, has launched the mainnet of Margin Trade, its new on-chain perpetual trading platform

Margin Trade is a Solana native, on-chain perpetuals trading platform that aims to bridge crypto native on chain trading with traditional finance (TradFi) instruments in a unified environment, making it possible for users to trade different asset classes, including cryptocurrencies, commodities such as silver and gold, and synthetic equity indices, all in one place.

By leveraging Solayer’s low-latency InfiniSVM infrastructure, Margin Trade delivers high-performance on-chain trading, enabling traders to benefit from real-time trade execution, high throughput, low fees, full transparency, and self-custody of their assets.

“Most perpetual futures trading infrastructure today remains siloed across separate markets and fragmented collateral account structures,” said Joshua Sum, Solayer’s Chief Product Officer.

“Margin Trade is designed to bring capital efficiency, real-time execution, and multi-asset exposure into a unified environment that feels closer to the vision of truly global financial markets than traditional trading platforms.”

Margin Trade is being developed by a team of professionals, including former traders from leading financial institutions and crypto exchanges such as Citadel and Kraken. The platform combines the speed and efficiency of centralized exchanges with the transparency, permissionless nature, and self-custody principles of decentralized finance (DeFi).

About Solayer

Solayer, also known as Solayer Labs, is a blockchain infrastructure company building a next-generation execution layer for real-time financial applications. Its goal is to create on-chain infrastructure that matches or exceeds the speed and performance of traditional financial systems.

Since its launch in 2023, the Solayer team has raised $12 million in funding. The company has also launched InfiniSVM, a hardware-accelerated Layer 1 blockchain built on the Solana Virtual Machine (SVM). According to the company, the network is capable of achieving up to 1,000,000 transactions per second and throughput exceeding 100 Gbps.

Margie Feng, Solayer’s Head of Marketing, is also scheduled to speak at the upcoming Rare Evo 2026 conference, which will be held from July 28 to July 31 this year.

Cash App Goes Live With USDC For 60M Users

Block's Cash App has officially begun rolling out USDC stablecoin payments to its nearly 60 million monthly users. The feature went live today for roughly 25% of the platform's user base, with full availability expected by the end of the week.

The rollout covers four blockchain networks: Solana, Ethereum, Polygon, and Arbitrum. Users can now send USDC from their Cash App wallet to external wallets on any of the supported chains, and incoming USDC is automatically converted into a dollar balance within the app. No separate transfer fee applies, at least for now.

A Reluctant Pivot, Years in the Making

The launch carries some ideological weight. Jack Dorsey, Block's CEO and longtime Bitcoin maximalist, spent years positioning Cash App as a Bitcoin-first platform. He built out Bitcoin trading, backed mining hardware development, and integrated Lightning Network support for Square merchants globally. Stablecoins were not part of that vision.

That changed, grudgingly. In March, Dorsey publicly acknowledged the shift. "I don't like that we're going to support stablecoins but our customers want to use them," he said. "I don't think it's wise to go from one gatekeeper to another." The comment was candid in a way that's rare for major fintech announcements, and it framed the product addition less as strategic enthusiasm and more as a concession to market demand.

Block first hinted at the feature on the Cash App website late last year, describing stablecoins strictly as a payments mechanism rather than an investment tool. But that early hint has carried through to the live product.

Why Solana (and Why Not Just Solana)

Solana started as the sole chain involved with Cash App. Back in November 2025, Solana confirmed its involvement after sharing a demo by Circle's Jeremy Allaire showcasing a USDC transfer on the network. The choice made sense: Solana transactions typically cost under a cent and settle in under a second, conditions well-suited for the kind of peer-to-peer and remittance use cases Cash App serves.

But Block's Miles Suter framed the company's stance as "chain- and coin-agnostic" from the beginning. Solana was a starting point, not a commitment. The live rollout now includes Ethereum, Polygon, and Arbitrum alongside Solana, giving users flexibility across networks with different cost and speed profiles. Ethereum's gas fees can still spike during congestion, which is precisely why Layer 2 options like Arbitrum and Polygon matter.

The multi-chain approach also future-proofs the integration somewhat. If one network faces congestion or reliability issues at scale, users and the platform aren't locked in.

The Guardrails Are Real

Cash App is not positioning this as a DeFi on-ramp. The feature comes with meaningful restrictions. Sending is capped at $2,000 per day and $5,000 per week; receiving tops out at $10,000 weekly. The service is currently unavailable in New York and on sponsored accounts. Identity verification is required.

Perhaps most importantly, the app warns users that blockchain transactions are irreversible. Funds sent to a wrong address or unsupported network are gone permanently. That's a steep hill to climb for a consumer platform serving tens of millions of people who may be encountering on-chain transfers for the first time.

Stablecoins Are Here To Stay...and Thrive

Cash App's move lands against a backdrop of surging stablecoin adoption. As of this week, the total market value of stablecoins has hit a record $322 billion, exceeding the foreign exchange reserves of 95 nations, including the UK and Canada. USDC, issued by Circle, is the second-largest stablecoin and already sees over $14 billion in liquidity on Solana alone.

Western Union launched Solana-based remittances in the first half of 2026. Stripe has added USDC support across multiple chains. Visa has integrated Solana for stablecoin settlements. The regulatory picture has also clarified somewhat, with the GENIUS Act signed in July 2025 establishing a clearer federal framework for stablecoin issuance.

Taken together, this feels less like a novelty launch and more like a platform making its peace with where consumer payments are heading. Dorsey may not love it, but the product is live, the networks are there, and 60 million people now have a relatively frictionless path to on-chain dollar transfers whether they know what a blockchain is or not.

Flipcash and Coinbase Launch USDF Stablecoin

Flipcash, a digital payment app founded by Ted Livingston, the founder of messaging app Kik, has partnered with Coinbase to launch USDF, a stablecoin pegged to the U.S. dollar.

According to Coinbase, the launch aims to make stablecoin issuance more accessible. Through the partnership, Flipcash can leverage Coinbase’s custom stablecoin platform to create its own stablecoin asset without having to handle much of the underlying technical complexity itself. As a result, Flipcash does not need to build an entire stablecoin infrastructure from scratch.

The USDF stablecoin will be issued on the Solana blockchain and will be 1:1 backed by USDC. It will also serve as Flipcash’s native currency. Since Flipcash allows users to create their own digital currencies, USDF will be the asset in which those currencies are priced and settled. It will serve as the settlement asset for trading digital currencies within the Flipcash app.

Coinbase’s Custom Stablecoin Platform

Coinbase custom stablecoin, or stablecoin as a service, is a platform launched by Coinbase in 2025 that allows businesses to easily create and issue their own branded stablecoins backed by the United States dollar.

As the stablecoin market continues to grow and gain institutional adoption, Coinbase launched its stablecoin platform to make it easier for businesses to enter the stablecoin market, reducing the technical and compliance work associated with issuing stablecoins.

Stablecoins launched on Coinbase’s custom stablecoin platform, including USDF, which is the first stablecoin created on the platform, will maintain a 1-to-1 backing with USDC and will be supported across multiple chains, including Base and Solana.

About Flipcash

Flipcash is a Solana-based non-custodial mobile wallet and digital payment app created by Canadian entrepreneur Ted Livingston in 2021.

It was created to digitize cash and make peer-to-peer payments as frictionless as possible. Through its “Currency Creator” feature, which officially went live last month, Flipcash allows anyone to create a fixed supply of digital currencies.

Wall Street Is Going To Tokenize Everything

There was a version of this story...told many moons ago that gets told as a prediction. Some future moment when the old guard of finance finally meets crypto on equal footing, when the suits and the degens find common ground, when a BlackRock executive and a DeFi protocol share the same balance sheet. Well that story is now pretty outdated...it's no longer some vision of an oracle peering into a crystal ball. We are already living in it. The future is here.

What we are seeing happen in global finance with tokenization is not some pilot program or a hedge. It is a structural transformation, and it is accelerating faster than most people outside of these two worlds seem to understand. Wall Street is no longer on the outside looking in, just dipping their toes in, to test the water. They have taken the plunge.

The Old System Was Always Broken

Here is something traditional finance never really wanted to say out loud: the infrastructure holding it together is ancient, slow, and held up largely by institutional inertia. Settlements that take days. Liquidity locked to six-and-a-half-hour trading windows. Layers of intermediaries, each one clipping a fee, each one adding time. For the largest players, those inefficiencies were baked into the cost of doing business. For everyone else, especially retail investors in markets outside the U.S., they were just walls.

Blockchain does not fix all of this overnight. But it offers something that legacy systems fundamentally cannot: a shared, programmable, real-time record of ownership that does not require three middlemen to reconcile. The World Economic Forum, in its 2025 report on asset tokenization, described the transition as potentially the next major phase in the development of financial market architecture, drawing a comparison to the shift away from paper certificates in the 1960s. That is not a crypto inside touting to his followers on X. That is the WEF stating how tokenization could transform finance.

When even the most establishment-facing institutions are framing this as a generational infrastructure shift, it's probably worth paying attention to.

The Institutions Are Not Coming. They Are Here.

BlackRock has a tokenized fund on Ethereum. JPMorgan launched a second tokenized money market product backed by U.S. Treasuries. Fidelity brought its own Digital Interest Token on-chain. Franklin Templeton has been quietly building its tokenized money market fund, BENJI, across multiple blockchains for years. These are live products managing real capital.

The total market for tokenized real-world assets crossed $75 billion in 2025. Projections from market analysts put the long-term ceiling at $18.9 trillion by 2033, and some estimates, citing the total addressable market of traditional finance, go much higher. Larry Fink has publicly stated, more than once, that he believes every financial asset can eventually be tokenized. When the CEO of the world's largest asset manager says that with conviction, the rest of the industry listens.The total crypto market sits at just shy of $2.6 trillion right now, to add some perspective to the type of volume tokenization can bring to the space.

And the whole idea behind this is not ideological. It is practical. Blockchain cuts settlement time, removes redundant intermediaries, enables fractional ownership, and allows assets to be composable across different financial products. For institutions moving hundreds of billions, those efficiency gains compound into something very significant, very quickly.

xStocks and the Part Where It Gets Really Interesting

Tokenized treasuries and money market funds are the institutional on-ramp. But the development that best captures where all of this is truly heading is xStocks, and it is worth understanding why it matters as much as it does.

Launched in June 2025 by Backed Finance, a Swiss RWA issuer, xStocks put more than 60 fully collateralized U.S. equities on Solana as SPL tokens. Apple. Tesla. Nvidia. Amazon. Each one backed 1:1 by real shares held under regulated custody. Not synthetic. Not a derivative. The actual stock, on-chain. Available the same day on Kraken and Bybit to users in over 185 countries, and within hours, live across Solana's DeFi ecosystem on Raydium, Jupiter, and Kamino.

The numbers since launch have been hard to argue with. Over $25 billion in total transaction volume. More than 80,000 unique on-chain holders. The platform has since expanded to 100 fully backed listings, and xStocks recently launched xChange, a unified execution layer for tokenized equities running 24/5 across Ethereum and Solana with atomic settlement built in. And we'll go back to the numbers. xStocks is amazing. It's done over $25 billion in volume. But daily stock market volume just in the U.S. is roughly $500-700 billion. Daily. Just in the U.S. Starting to get the big picture here? The much, much bigger picture?

What makes this genuinely different from everything that came before it is composability. With a brokerage account, you own a stock and that is more or less the end of the story. With xStocks inside Solana's DeFi ecosystem, you can use Nvidia as collateral in a lending protocol, provide liquidity with Apple against a stablecoin, or swap Tesla for SOL without touching a broker, a clearinghouse, or a trading window. That kind of programmable financial infrastructure does not exist in traditional markets. It simply never has.

Who This Actually Opens the Door For

For investors in the U.S., this is interesting. For investors everywhere else, it is potentially transformative. Access to U.S. equity markets has historically required meeting regulatory hurdles, working through licensed brokers, and navigating banking infrastructure that many parts of the world simply do not have. xStocks changes that math entirely. Trading starts at one euro. Dividends reinvest automatically. No broker required. No minimum account size. Just a wallet and a connection.

Franklin Templeton's partnership with Kraken, announced in early 2026, is another data point worth noting here. The two are exploring on-chain versions of Franklin's financial products, including tokenized stocks, yield instruments, and compliant custody solutions. A legacy asset manager and a crypto exchange building joint infrastructure is the kind of thing that a few years ago would have sounded like a very optimistic projection. Now it is a press release.

The Narrative Has Shifted. Permanently.

Crypto spent a long time fighting to be taken seriously by traditional finance. That fight is over, and crypto won it on the merits. What is replacing it is something more interesting: a negotiation over what the merged system actually looks like, who controls it, and how fast it scales.

The regulatory environment is improving. Interoperability between chains is being worked out. Liquidity in tokenized asset markets is growing month over month. The WEF framed the barriers as real but solvable, pointing to legacy infrastructure integration, inconsistent global standards, and cross-chain friction as the remaining friction points. None of those are permanent problems. They are engineering and coordination challenges, and the talent and capital now focused on solving them is enormous.

The General Manager of xStocks said it about as cleanly as it can be said: the question is no longer whether equities belong on-chain, but how fast they can be scaled. With 100 listings and $25 billion in volume already behind the platform, the model is proven. The next stage is expansion to every major U.S. equity and, eventually, global equities across international markets.

That is not a roadmap for some distant future version of crypto. That is the roadmap for the next few years. And if the last twelve months are any indication, it will probably move faster than anyone is currently projecting, including myself. As bullish as I am on all of this, I have a feeling that the transition to tokenize the world will be bigger than anything I could ever imagine.

KRWQ Stablecoin Expands to Solana for KRW Trading

KRWQ, a stablecoin pegged to the South Korean won, is expanding to Solana following a recent announcement from IQ, the company behind the stablecoin.

The expansion, according to IQ, is aimed at enhancing KRWQ support for various Korean won-denominated trading applications on Solana, including perpetual futures, on-chain foreign exchange markets, arbitrage strategies, cross-margin trading, and other institutional and algorithmic trading systems and applications.

“The Korean won is a major global currency with substantial activity in offshore derivatives markets, yet it has remained largely inaccessible in crypto native trading systems,” IQ said in a statement to reporters. “KRWQ allows market participants to trade, hedge, and deploy capital using Korean won liquidity directly on chain.”

Regarding its decision to launch KRWQ on Solana, the IQ team cited Solana’s low latency and deep liquidity as key reasons for selecting the network.

“Solana provides the performance and ecosystem depth needed to scale KRW liquidity on chain,” said Dave Shin, chief operating officer of KRWQ. “We are seeing clear demand for non-USD trading pairs, particularly in derivatives.”

As KRWQ’s adoption continues to grow among both retail and institutional users, IQ expects increased usage of the stablecoin across a wide range of applications, including cross-border settlements and advanced trading systems.

About the KRWQ stablecoin

KRWQ is a stablecoin developed by IQ in collaboration with Frax Finance, a notable decentralized finance project. It was created with the main goal of bringing the Korean won (KRW) onto the chain.

By enabling 24/7 trading, instant settlement, and low-cost on-chain transactions, KRWQ addresses major inefficiencies in offshore KRW trading, increasing demand for and use of KRW in global payments and decentralized finance, while reducing dependence on US dollar-pegged stablecoins.

Since its launch in October 2025, KRWQ has rapidly gained traction as the first on-chain settlement layer for Korean won trading, expanding beyond Base, its initial deployment chain, and going live on Fraxtal, Codex, Morph, and Hydrex. KRWQ was also recently listed on EDX Markets, an institutional-focused cryptocurrency exchange, across spot and perpetual futures.

KRWQ now has a spot trading volume of nearly $40 billion and a Non-Deliverable Forward (NDF) market worth about $60 billion.

Jupiter, Bitwise Launch Institutional USDe Lending Market

Jupiter, the Solana-based decentralized finance platform, has partnered with crypto asset manager Bitwise Asset Management and decentralized lending infrastructure protocol Fluid to launch an Ethena (USDe) focused lending market on the Jupiter platform.

The partnership will see the launch of an institutional grade USDe lending market on Jupiter’s lending platform, with Bitwise serving as the curator of the new market, setting risk parameters and overseeing operations, while Fluid powers the lending infrastructure.

By assigning USDe lending curation responsibilities to Bitwise, a traditional finance asset management firm, Jupiter aims to achieve institutional grade credibility and easier access to large scale institutional capital, with the potential for the market to grow into the billions of dollars.

“USDe is an institutional grade savings product built for scale. By combining Jupiter Lend's advanced lending infrastructure with Bitwise's asset management expertise, we have created an efficient USDe market ready for DeFi and institutional adoption,” said Guy Young, founder and chief executive officer of Ethena Labs.

Before now, institutional capital and DeFi lending mostly operated separately. However, with the launch of this USDe lending market for institutional access, all entities involved, including TradFi and DeFi participants, can work together: Jupiter providing the lending market, Bitwise curating the market, Ethena supplying the asset, and Fluid powering the infrastructure.

“Now more than ever, it is imperative that we take DeFi risk seriously. That is precisely why we are excited to partner with Bitwise, who bring both the expertise and the institutional credibility needed to help scale on chain lending from a niche into the default way to do finance,” said Kash Dhanda, chief operating officer of Jupiter.

“And by working with Ethena and Fluid, two of the most technically innovative teams in the space, we are thrilled to deliver a product experience like no other.”

Institutions Double Down on DeFi

With DeFi growing rapidly and its TVL reaching new highs of around $150 billion to $225 billion in 2025, there has been an increase in the number of institutions entering and doubling down on DeFi.

Institutional capital reportedly made up around 11.5% to 20% of DeFi volume or lending TVL in parts of 2025, with institutions like BlackRock, Bitwise, and JPMorgan Chase doubling down on real world asset tokenization and stablecoins.

Meta Tests USDC Stablecoin Payouts for Creators

Social media giant Meta is currently running a pilot program that tests issuing creators’ payouts in stablecoins. “Meta now offers USDC stablecoin payouts via supported crypto wallets on the Solana and Polygon blockchain networks,” the team wrote on its Business Help Center page

Since this is still a pilot program, only creators in Colombia and the Philippines are currently eligible for the service, with the program expected to expand to more than 160 countries before the end of the year, according to an X post by Polygon Labs.

While the announcement was well received by many in the crypto community, a spokesperson for Meta clarified the goal of the initiative, stating that Meta was not issuing its own stablecoin but was instead tapping into Circle’s $77 billion USDC stablecoin, with plans to integrate the stablecoin into its payment infrastructure.

The Meta USDC creator payout program is currently supported by several popular crypto wallets, including MetaMask, Phantom, and Binance, with global payments platform Stripe handling the technical infrastructure and serving as the payments provider. Solana and Polygon are the only blockchain networks currently supported for this program.

Meta Pushes Again Into Crypto After Setbacks

Meta’s recent move into crypto follows several setbacks it has had to deal with in the past. In 2019, it launched Libra, a cryptocurrency which it said could be used across its different social media platforms, including Facebook, Instagram, and WhatsApp.

However, things did not go as planned, as some stakeholders, such as PayPal, Mastercard, and Visa, which were involved in the project, started pulling out due to scrutiny and backlash from U.S. regulators and from some members of the U.S. Congress.

Although Meta made several efforts to save the project, including rebranding it from Libra to Diem, a stablecoin backed by the U.S. dollar in an effort to appease federal regulators, nothing worked, as federal regulators stated that the project could not move forward.

Other projects associated with Libra and Diem, such as the Novi wallet, a cryptocurrency wallet built by Meta that allowed users to hold and transfer Libra, also failed, and the entire project was eventually wound down. According to Stuart Levey, then CEO of the Diem Association, “it became clear from our dialogue with federal regulators that the project could not move ahead.”

OKX Launches AI Agent Payments Protocol for Crypto Commerce

Cryptocurrency exchange OKX has launched Agent Payments Protocol (APP), a new payment protocol that allows AI agents to perform commercial activities.

The new payment protocol, according to OKX, is an open standard that defines how AI agents communicate and negotiate, pay for services, and pay each other. It also, for the first time, allows AI agents to move beyond simple payments and into full-scale commerce.

“In the past few months, AI agents moved from answering questions to running workflows, managing business processes, and acting autonomously on behalf of users,” OKX wrote in a blog post. “The bottleneck shifted from intelligence to commerce - not just paying, but the full cycle of doing business: quoting, negotiating, escrowing funds, metering usage, settling, and resolving disputes.”

This existing problem among AI agents is what OKX aims to solve with its new Agent Payments Protocol (APP), allowing agents not only to manage single payment requests but also to manage payment requests across multiple levels.

Inside the Agent Payment Protocol

The agent payment protocol (APP) from OKX is an open standard designed to work across all chains, especially the Solana and Ethereum blockchains.

APP unlocks new capabilities for AI agents, making it possible for these agents to operate and communicate autonomously across the full commerce lifecycle, pay each other through agent-to-agent payments, and also allowing AI agents to perform upfront and top-up payments, including deductions.

At its implementation layer is the payment software development kit (SDK) that makes it possible for developers to accept and make agent payments with just a few lines of code. According to the blog announcement, the agent payment protocol supports a wide variety of payments, including one-time payments, batch payments, pay-as-you-go, and escrow payments, which OKX says is coming soon.

Embedded within the payment protocol is the OKX self-custodial agentic wallet, which supports over 20 blockchains. Since the wallet is secured by means of a Trusted Execution Environment (TEE), a hardware-based security environment, the wallet’s private keys and sensitive operations are kept highly secure.

Despite its early launch, the OKX agent payment protocol is currently supported by major cloud infrastructure firms, including Amazon Web Services (AWS) and Alibaba Cloud, as well as blockchain companies such as Uniswap, Paxos, MoonPay, Zerion, and Nansen.

With the launch of its payment protocol, OKX joins companies such as Coinbase, Stripe, and OpenAI, which have already launched their payment protocols, namely x402, Agentic Commerce Protocol (ACP), and Machine Payments Protocol (MPP), respectively.

Western Union to Launch USDPT Stablecoin on Solana

Global financial services company Western Union has announced its plans to launch its long awaited U.S. Dollar Payment Token (USDPT) stablecoin next month.

The Solana based USDPT stablecoin, which is to be issued by crypto bank Anchorage Digital, is already in its final stages of preparation and is expected to launch, Devin McGranahan, Western Union CEO and President, revealed during the firm’s recent first quarter earnings call.

"It is no longer a question of if Western Union will be active in digital assets; it is now how fast we can scale," McGranahan said during the call with investors and financial analysts.

McGranahan also revealed in a Q&A session that the USDPT stablecoin will not be launched as a consumer product, but will instead initially be used internally as an alternative to the SWIFT network. With the USDPT stablecoin, Western Union aims to facilitate fast transaction settlements in real time with its agents around the world.

Other Services to Be Launched Alongside USDPT

Alongside the USDPT stablecoin, Western Union will be launching two additional services and products: its USD stablecard and the Digital Asset Network, or DAN, which allows digital assets, including USDPT and crypto wallets, to connect with Western Union’s existing infrastructure.

By means of a single connection to Western Union’s API, DAN provides off ramp services to users, enabling them to convert stablecoins held in crypto wallets into local currencies.

"Through DAN, millions of wallet users will be able to move from digital assets into local currency using Western Union's retail network, with an experience that is simple for customers and familiar for our agents," McGranahan said, while also stating that the first partner of the network will be revealed next week. DAN will be made available in over 360,000 locations across more than 200 countries and territories.

To allow users to hold value in stablecoins, including USDPT, Western Union will also be launching its USD stablecard, a consumer based card developed by crypto wallet provider Rain and Visa.

The stablecard, according to McGranahan, will be especially compelling in inflation sensitive markets where customers want dollar denominated value, and it will be launched across dozens of markets worldwide. With the card, users living in areas hit by high inflation will be able to hold USD based stablecoins and spend them globally.

Tokenized Stocks Hit $1B Market Cap Milestone

Tokenized stocks have crossed the $1 billion market cap marking a major turning point for RWAs on-chain. Public equities drove the surge, with platforms like Ondo Global Markets and xStocks leading the charge, while tokenized private equities on Solana continue to gain early traction and expand rapidly.

The rise of tokenized stocks brings several benefits to investors as they enable 24/7 global trading without the traditional T+2 settlement delays, allowing markets to operate continuously rather than shutting down after regular hours. Fractional ownership lowers the barrier for smaller investors to gain exposure to stocks and private investments. Assets can be used directly as collateral in DeFi protocols, creating new opportunities for yield generation and liquidity with instant settlement that reduces counterparty risk and improves capital efficiency.

Ondo Finance and xStocks together account for over 90% of the tokenized stock market cap. Ondo leads at $741.1M (heavily on Ethereum at $440.1M and BNB Chain at $283.2M), followed by xStocks at $315.2M (dominant on Solana with $258.4M and reach through CEXs like Kraken and Bybit). The rest includes Superstate, Robinhood on Arbitrum, Dinari, and PreStocks’ $17.8M in tokenized private equities. Launched in June 2025, xStocks has already facilitated over $3.5 billion in on-chain transaction volume and $25 billion in total trading volume, tokenizing major assets like SPYx, QQQx, NVDAx, and TSLAx.

Another interesting segment is tokenized pre-IPO stocks that bring exposure to private companies like Anthropic directly onto Solana via platforms such as PreStocks. These tokens are created through Special Purpose Vehicles (SPVs) that hold shares or exposure acquired on secondary markets. PreStocks then issues 1:1 backed SPL tokens on Solana that track the company's implied valuation which lets holders get price exposure with 24/7 trading on DEXes like Jupiter. The tokenized pre-IPO sector has grown roughly 200% year-to-date, with Anthropic leading the surge.

However, Ethereum is still the clear leader when it comes to bringing stocks on-chain, as it’s become the primary home for major financial moves as the value of funds moving onto Ethereum has grown 20x since the start of 2024, thanks to massive names like BlackRock and Fidelity launching their own products there. This dominance extends across other major real-world asset categories as well, with the network maintaining a strong position in tokenized commodities, funds, and stablecoins.

Nasdaq has secured SEC approval to trade tokenized Russell 1000 stocks and major index ETFs on the same order book as their traditional counterparts, while the NYSE is building a 24/7 on-chain venue with instant settlement and stablecoin funding in partnership with Securitize and the DTCC’s tokenization infrastructure. Firms like Franklin Templeton, JPMorgan, and Apollo are rolling out tokenized money market funds, credit strategies, and other securities across networks that reache beyond Ethereum and Solana to include chains like Polygon, Avalanche, Base, Aptos, and Stellar, reflecting a multi-chain strategy to plug directly into different DeFi ecosystems.

Ondo Global Markets, now one of the main issuers of tokenized U.S. stocks and ETFs, blocks U.S. users and anyone trading from inside the country, and pushes those restrictions through partners like MetaMask, Binance Wallet, and centralized exchanges that list its products. Kraken’s xStocks do the same, limiting access to non U.S. clients in a set list of jurisdictions and explicitly excluding residents of the United States, Canada, the U.K., and Australia. On Solana, the pre-IPO names led by PreStocks let people trade tokens linked to companies like Anthropic, but they sit in a gray zone because they’re SPV based claims with no audited, public proof of backing, wide gaps between implied token prices and private round valuations, thin liquidity, and no clear path for U.S. retail to participate. So while Binance, OKX, Kraken, and others rush to put tokenized stocks in front of millions of users, most of the real volume is still offshore, and U.S. investors are mostly stuck watching from the sidelines until policy catches up.